SBR INT – Chapter 2: The financial reporting framework

The financial reporting framework

Key Points to Highlight in Chapter 2

- International Financial Reporting Standards (IFRS):

- Developed and issued by the International Accounting Standards Board (IASB).

- Aim to standardize financial reporting practices globally.

- Provide principles-based framework for financial reporting.

- Used by multinational companies for consolidation purposes.

- Generally Accepted Accounting Principles (GAAP):

- Developed and issued by the Financial Accounting Standards Board (FASB) in the United States.

- Mandatory for listed companies in the United States.

- Legally binding for companies operating in jurisdictions where GAAP is mandated.

- More rules-based compared to IFRS.

- European Financial Reporting Standards (EFRS):

- Specific to financial reporting in the European Union.

- Provides guidelines and standards for reporting by EU-based companies.

- Regulatory Oversight:

- Securities and Exchange Commission (SEC) oversees GAAP adoption in the United States.

- European Securities and Markets Authority (ESMA) oversees IFRS adoption in the European Union.

- International Accounting Standards Board (IASB) oversees IFRS adoption globally.

- Differences:

- GAAP: Used primarily in the United States, rules-based, mandatory for listed US companies.

- IFRS: Used globally, principles-based, promotes comparability and consistency.

- EFRS: Specific to EU, provides guidelines for EU-based companies.

- Flexibility and Interpretation:

- IFRS allows for more flexibility and interpretation in financial reporting compared to GAAP.

- IFRS aims to promote consistency and comparability while accommodating diverse business practices.

Topic 1: The Applications, Strengths, and Weaknesses of an Accounting Framework

The financial reporting framework provides a critical foundation for creating a consistent and informative picture of an entity’s financial performance and position. Understanding its applications, strengths, and weaknesses is crucial for accountants, analysts, and other stakeholders who rely on financial statements. This section dives deep into the core components of the framework, exploring various theories and illustrations to solidify the concepts.

A) Importance of the Conceptual Framework for Financial Reporting in Underpinning the Production of Accounting Standards:

The Conceptual Framework for Financial Reporting (Conceptual Framework), developed by the International Accounting Standards Board (IASB), serves as the foundation for International Financial Reporting Standards (IFRS). It establishes fundamental principles and concepts that guide the development and application of accounting standards.

Importance:

- Consistency: Ensures a uniform and consistent approach to financial reporting across different entities and industries.

- Decision-making: Provides a common language for financial statements, enabling users to compare and interpret information from different companies.

- Flexibility: Offers a flexible framework adaptable to new and emerging financial instruments and transactions.

- Reduction of judgment: Reduces the need for individual judgment by established guidelines and principles.

Illustration: The Conceptual Framework defines the elements of financial statements, such as assets, liabilities, equity, income, and expenses. These definitions are then used in developing specific IFRS on recognizing, measuring, and disclosing these elements in financial statements.

B) Objectives, Principles, and Limitations of Financial Reporting:

Objectives:

- Provide financial information used by users (investors, creditors, analysts, etc.) to make informed economic decisions.

- Demonstrate accountability and stewardship for the management of resources entrusted to the entity.

- Promote transparency and comparability of financial information across different entities.

Principles:

- Accrual accounting: Recognizes transactions and events affecting the financial position and performance in the period they occur, regardless of cash flow.

- Going concern: Assumes the entity will continue operating in the foreseeable future.

- Matching principle: Expenses are recognized in the same period as the revenue they generate.

Limitations:

- Subjectivity: Certain aspects of financial reporting require judgment and interpretation, leading to potential inconsistencies across entities.

- Emphasis on the past: Financial statements primarily reflect past events and transactions, offering limited future prediction capabilities.

- Incompleteness: Certain qualitative factors like corporate reputation or employee morale are not directly captured in financial statements.

Illustration: The objective of providing information for informed decision-making necessitates presenting financial information in a clear, concise, and understandable manner. This involves adhering to presentation and disclosure principles, such as true and fair view, materiality, and going concern.

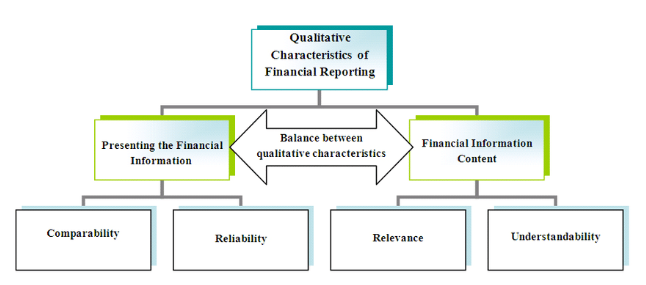

C) Qualitative Characteristics of Useful Financial Information:

The Conceptual Framework outlines qualitative characteristics that enhance the usefulness of financial information for decision-making. These characteristics act as guiding principles in the preparation and presentation of financial statements.

Key Characteristics:

- Relevance: Information is capable of making a difference in the decisions of users.

- Reliability: Information is faithful and free from material error.

- Comparability: Information allows users to compare the financial position, performance, and cash flows of different entities over time.

- Understandability: Information is presented in a clear and concise manner, readily understandable by users with a reasonable knowledge of business and financial accounting.

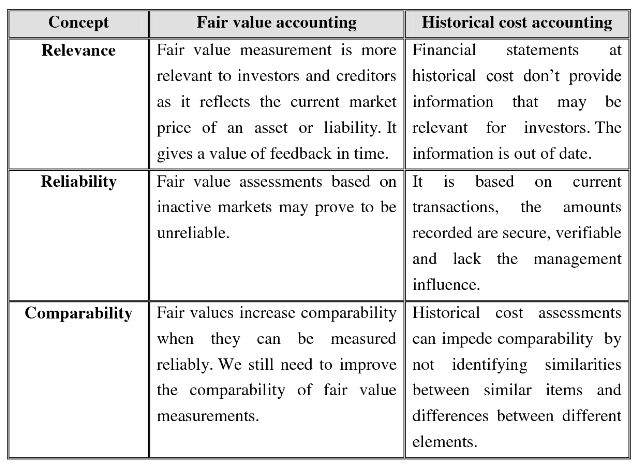

Illustration: When valuing an inventory item, the accountant might consider multiple valuation methods (e.g., first-in, first-out (FIFO) or last-in, first-out (LIFO)). The chosen method should be relevant to the entity’s specific circumstances and provide reliable information for decision-making, while ensuring comparability with historical financial statements and industry peers.

D) Principles of Recognition, Derecognition, and Measurement:

The Conceptual Framework establishes the principles for recognizing, derecognizing, and measuring the elements of financial statements.

Recognition: An item is recognized when it meets the definition of an element and:

- It is probable that future economic benefits (income) or economic sacrifices (expenses) will flow to or from the entity; and

- The item can be measured reliably.

Derecognition: An item is derecognized when:

- The entity no longer controls the item; or

- The item no longer meets the definition of an element.

Measurement: The chosen measurement basis should be relevant to the users of financial statements and faithfully represent the underlying economic substance of the item. Common measurement bases include:

Common Measurement Bases:

- Historical cost: The initial cost of acquiring an asset.

- Current cost: The amount currently required to acquire the same or equivalent asset.

- Fair value: The price that would be received in an orderly exchange between willing buyer and seller.

Measurement Uncertainty:

Financial statements are inherently subject to measurement uncertainty, arising from:

- Estimates: Many components of financial statements rely on estimates and judgments (e.g., useful lives of assets, impairment losses).

- Incomplete information: Obtaining complete and accurate information about all aspects of an entity’s financial position is often challenging.

Materiality:

The principle of materiality states that information is considered material if its omission or misstatement could influence the decisions of users. Determining materiality involves professional judgment and depends on the specific circumstances.

Illustration: Recognizing and measuring property, plant, and equipment (PPE) involve applying these principles. An entity initially recognizes PPE at its historical cost. Subsequently, the entity may choose to measure PPE at historical cost less accumulated depreciation or fair value based on materiality and relevance considerations. Measurement uncertainty arises from estimating useful lives and impairment losses, requiring the application of professional judgment and materiality assessments.

E) Definitions of the Elements of Financial Statements and Reporting in the Statement of Profit or Loss and Other Comprehensive Income:

The Conceptual Framework defines the elements of financial statements, which are the basic building blocks of financial reporting. These elements include:

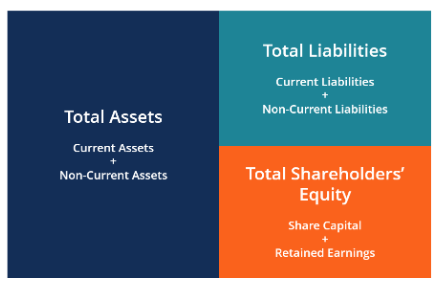

- Assets: Resources controlled by the entity with the expectation of future economic benefits.

- Liabilities: Present obligations of the entity arising from past events, the settlement of which is expected to result in an outflow of resources from the entity.

- Equity: The residual interest of the owners in the assets of the entity after deducting all its liabilities.

- Income: Inflows of assets during a period arising from ordinary activities of the entity.

- Expenses: Outflows of assets or incurrences of liabilities during a period arising from ordinary activities of the entity.

Statement of Profit or Loss and Other Comprehensive Income (SOPL/OCI):

The SOPL/OCI reports the financial performance of an entity during a period, categorizing income and expenses. Other comprehensive income (OCI) includes items of income and expense that do not meet the definition of profit or loss.

Illustration: The definition of revenue clarifies that it arises from the ordinary activities of the entity and represents the inflow of assets resulting from the sale of goods or services. In the SOPL, revenue is typically the first line item, followed by expenses categorized by nature (e.g., cost of goods sold, administrative expenses). The OCI section might report revaluation gains on property, plant, and equipment, which are not recognized in profit or loss but impact total comprehensive income.

Conclusion:

Understanding the applications, strengths, and weaknesses of the financial reporting framework is crucial for interpreting and utilizing financial statements effectively. The Conceptual Framework serves as the foundation for IFRS, providing a consistent and reliable framework for financial reporting, while acknowledging limitations and the need for judgment in certain situations. By understanding the qualitative characteristics of useful information and the principles of recognition, derecognition, and measurement, stakeholders can gain a deeper understanding of the information presented in financial statements and make informed decisions.