F1 – Chapter 1 – The business organization and its external environment

Key Concepts to Master in Chapter 1

Business Objectives and Stakeholders

Businesses primarily aim for profit maximization, serving as a metric for efficiency and success.

Internal stakeholders, particularly shareholders, as they have a vested interest in the company’s performance and decisions.

PESTLE Analysis

Political, Economic, Social, Technological, Legal, and Environmental factors collectively shape the business environment.

Government policies, economic conditions, societal trends, technological advancements, legal regulations, and environmental concerns influence business operations and strategies.

Company’s Mission Statement

A mission statement articulates the organization’s overall purpose and direction.

It guides decision-making, strategy development, and communicates the company’s identity to stakeholders.

Financial Statements

The balance sheet provides a snapshot of a company’s financial position, including assets, liabilities, and shareholders’ equity.

It helps stakeholders assess the company’s financial health and make informed decisions.

SWOT Analysis

SWOT analysis identifies internal strengths and weaknesses, as well as external opportunities and threats.

It informs strategic planning by leveraging strengths and opportunities while addressing weaknesses and threats.

Corporate Governance

Corporate governance ensures ethical business practices, transparency, and accountability within organizations.

It establishes frameworks to guide decision-making and protect stakeholders’ interests.

Stakeholder Theory

According to stakeholder theory, businesses should balance the interests of all stakeholders.

This includes shareholders, employees, customers, suppliers, communities, and the environment.

Globalization

Globalization expands market opportunities by facilitating international trade, investment, and collaboration.

It increases competition but also fosters innovation and growth.

Management Functions

Planning, Organizing, and Directing are essential management functions that guide decision-making and resource allocation.

Monitoring ensures performance aligns with objectives and facilitates corrective actions.

External Business Environment

The external environment encompasses factors beyond a business’s control, such as economic conditions, political stability, and technological advancements.

Adapting to changes in the external environment is crucial for long-term success.

Business Structures

Sole trader, partnership, and company limited by shares are common business structures with varying levels of liability and ownership arrangements.

Strategic Analysis Tools

PESTLE analysis, SWOT analysis, and Michael Porter’s Five Forces framework are strategic tools used to assess internal and external factors influencing business operations and competitiveness.

Franchise Business Model

The franchise business model offers advantages such as brand recognition and shared costs but may limit franchisee control over operations.

Outsourcing

Outsourcing involves contracting non-core activities to external parties to enhance focus, reduce costs, and access specialized skills.

Michael Porter’s Five Forces

Michael Porter’s Five Forces framework assesses industry competitiveness by analyzing the threat of new entrants, bargaining power of suppliers and buyers, threat of substitutes, and competitive rivalry.

1. The purpose and types of business organization

Introduction:

This chapter explores the fundamental aspects of businesses: their purpose and the various structures they adopt to function within their external environment. Understanding these is crucial for anyone interested in business, especially accountants who need to grasp the context within which financial information is generated.

The Purpose of Business Organizations:

Businesses exist for multiple purposes, but two main goals stand out:

a) Profit Maximization: While often portrayed as the sole objective, profit serves as a vital indicator of efficiency and a source of funds for growth and investment. However, it’s not always the primary focus, as we’ll see with other organization types.

b) Providing Goods and Services: This core function fulfills individual and societal needs, contributing to economic well-being and creating value for stakeholders.

Types of Business Organizations:

The legal structure a business adopts influences its operation, ownership, liability, and financial reporting. Here are the key types:

1. Sole Trader:

- Definition: Owned and managed by one individual with unlimited liability (personal assets liable for business debts).

- Advantages: Simple setup, complete control, tax benefits.

- Disadvantages: Limited financing options, vulnerability to owner’s health, limited growth potential.

- Examples: Freelancers, consultants, small shops.

2. Partnership:

- Definition: Owned and managed by two or more individuals who share profits and losses according to an agreement. Partners have unlimited liability unless it’s a Limited Liability Partnership (LLP).

- Advantages: Combined expertise, shared financing, tax benefits.

- Disadvantages: Potential disagreements, unlimited liability (except LLPs), complex profit-sharing structures.

- Examples: Law firms, accounting firms, medical practices.

3. Limited Company:

- Definition: A separate legal entity owned by shareholders who invest capital but have limited liability (only liable for their investment). Managed by a board of directors elected by shareholders.

- Advantages: Limited liability, access to capital through share issuance, ability to grow and attract talent.

- Disadvantages: Complex setup and regulations, potential conflicts between shareholders and management, double taxation (on company profits and dividends).

- Examples: Publicly traded corporations, private limited companies.

4. Cooperatives:

- Definition: Owned and controlled by members who benefit from the organization’s activities (not necessarily profit-focused).

- Advantages: Democratic decision-making, focus on member needs, potential tax benefits.

- Disadvantages: Complex governance structure, potential slow decision-making, limited growth potential.

- Examples: Worker cooperatives, agricultural cooperatives, housing cooperatives.

5. Public Sector Organizations:

- Definition: Established by government to provide public services, funded by taxes or user fees.

- Advantages: Non-profit focus, providing essential services, accountability to public.

- Disadvantages: Bureaucracy, political influence, limited flexibility.

- Examples: Hospitals, schools, government agencies.

Additional Considerations:

- Hybrids: Some organizations combine elements of different structures, like Limited Liability Partnerships (LLPs).

- Not-for-profit Organizations: While not focused on profit, they have similar structures and play a crucial role in society.

- Global Context: Business environments and legal frameworks vary across countries, impacting which structures are more common.

Theories and Illustrations:

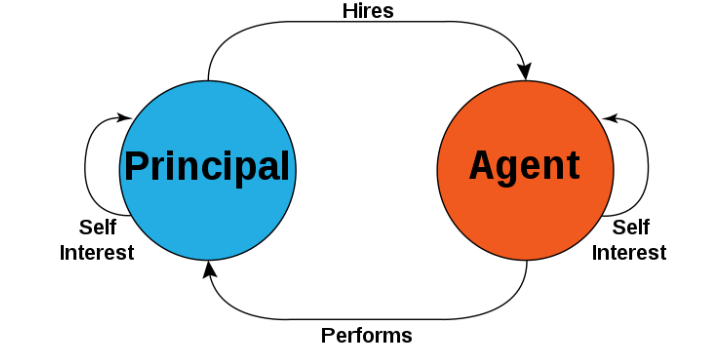

- Agency Theory: Examines the relationship between principals (owners) and agents (managers) within a company, exploring potential conflicts of interest and mechanisms for alignment.

Corporate Governance: In a publicly traded company, shareholders (principals) hire managers (agents) to run the company on their behalf. Agency theory explains the potential conflicts of interest that arise between shareholders and managers. For instance, managers might prioritize their own interests over those of the shareholders, leading to actions such as excessive risk-taking or empire-building.

Financial Advisory Services: When an individual hires a financial advisor to manage their investments, agency theory comes into play. The advisor is expected to act in the best interest of the client (principal) but may have incentives to recommend certain financial products that offer higher commissions, potentially conflicting with the client’s best interests.

- Stakeholder Theory: Recognizes the various groups (employees, customers, suppliers, community) affected by a business and emphasizes responsible decision-making that considers their interests.

Corporate Social Responsibility (CSR): Stakeholder theory suggests that companies should consider the interests of all stakeholders, not just shareholders. For example, a company might take actions to reduce its carbon footprint, benefiting not only shareholders but also employees, customers, and the environment.

Community Engagement: When a corporation engages with local communities in which it operates, it’s an application of stakeholder theory. For instance, a manufacturing company might initiate programs to support education or infrastructure development in the community, recognizing the importance of stakeholders beyond just shareholders.

- Transaction Cost Economics: Analyzes the costs associated with different organizational structures, helping choose the most efficient option for specific operations.

Make vs. Buy Decisions: In business, companies often face the decision of whether to produce a good or service in-house or to outsource it. Transaction cost economics helps analyze these decisions by considering factors such as the cost of negotiating and enforcing contracts, the risk of opportunistic behavior, and the costs of coordination. For example, a company might decide to outsource its IT support services if the transaction costs associated with hiring and managing in-house IT staff are higher than outsourcing to a specialized firm.

Vertical Integration: Transaction cost economics can explain the decision of firms to vertically integrate. For instance, a company might acquire its suppliers or distributors to reduce transaction costs associated with coordinating production, quality control, or distribution. By owning these entities, the firm can streamline operations and reduce the risks of opportunistic behavior by external parties.

Case Studies:

- Compare the ownership structure, decision-making processes, and challenges faced by a family-owned business vs. a multinational corporation.

- Analyze how a non-profit organization balances its social mission with financial sustainability.

- Discuss how government regulations impact the operations and growth of different types of businesses.

2. Stakeholders in business organizations

Introduction:

No business operates in isolation. Every organization exists within a complex ecosystem of individuals and groups with vested interests, known as stakeholders. Understanding these stakeholders, their expectations, and the dynamics of their interactions is crucial for sustainable success.

Who are Stakeholders?:

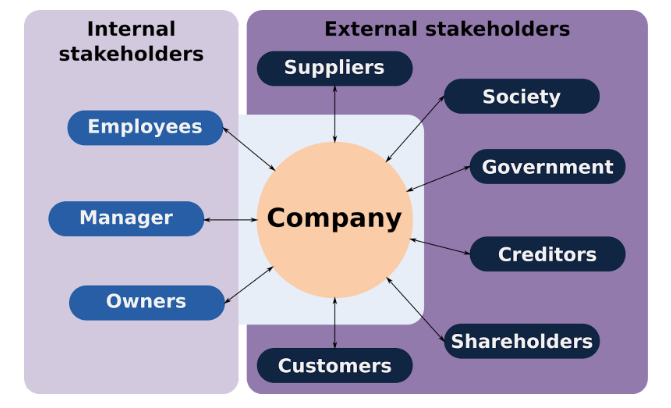

Stakeholders can be defined as any individual or group affected by, or influencing, the activities of a business. They can be internal or external:

Internal Stakeholders:

- Employees: Their skills, dedication, and well-being contribute directly to the organization’s performance.

- Management: Responsible for directing operations, making decisions, and ensuring the organization’s success.

- Shareholders/Owners: Owners of the company (in limited companies) with an interest in profit and capital appreciation.

External Stakeholders:

- Customers: Purchase goods and services, driving revenue and shaping the organization’s offerings.

- Suppliers: Provide resources and materials essential for production and operations.

- Creditors: Lend money to the organization, expecting timely repayment and interest.

- The Community: Impacted by the organization’s environmental, social, and economic activities.

- Government: Sets regulations and policies that guide and influence business operations.

- Media: Influences public perception and can impact reputation and stakeholder behavior.

Theories and Illustrations of Stakeholder Management:

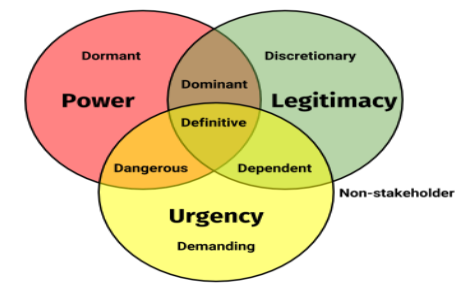

- Stakeholder Salience Model: Classifies stakeholders based on their power (ability to influence the organization) and legitimacy (perceived right to make claims). High-salience stakeholders require close attention and management.

Oil Company and Environmental Activists: Consider an oil company planning to drill in a sensitive environmental area. The stakeholders involved might include local communities, environmental activists, shareholders, regulatory agencies, and indigenous groups. The company would use the stakeholder salience model to analyze the power, legitimacy, and urgency of each stakeholder’s claims. Environmental activists might have high salience due to their power to mobilize public opinion and their urgent concerns about ecological damage, leading the company to engage with them through dialogue or mitigation efforts.

Technology Company and Privacy Advocates: A technology company developing a new data collection tool would need to consider the concerns of privacy advocates. These advocates may have high salience due to the legitimacy of their concerns about data privacy and the urgency of addressing potential privacy violations. The company might engage with them through transparency measures, privacy controls, or consultations to address their concerns.

- Stakeholder Theory: Argues that businesses should consider the interests of all stakeholders, not just shareholders, for long-term success and social responsibility.

Corporate Social Responsibility (CSR) Initiatives: Stakeholder theory suggests that companies should consider the interests of all stakeholders, not just shareholders. For example, a retail company might implement fair labor practices in its supply chain, benefiting workers, suppliers, customers, and the community at large.

Employee Welfare Programs: Companies that prioritize stakeholder theory often invest in employee welfare programs such as health insurance, training and development opportunities, and work-life balance initiatives. By valuing their employees as stakeholders, these companies aim to foster loyalty, productivity, and long-term success.

- Triple Bottom Line (TBL): Emphasizes measuring performance beyond financial profits to include social and environmental impact, reflecting stakeholder concerns.

Renewable Energy Company: A renewable energy company that measures its success not only by financial profit but also by its environmental impact and social responsibility exemplifies the triple bottom line approach. Such a company might focus on reducing carbon emissions, promoting sustainable practices in its operations, and investing in community development projects.

Social Enterprises: Social enterprises, which aim to address social or environmental issues while also generating profit, embody the triple bottom line concept. For instance, a company that produces and sells reusable products to reduce plastic waste not only generates financial returns but also contributes to environmental sustainability and community well-being.

Case Studies:

- Analyze how a company manages employee relations during a restructuring to balance stakeholder interests.

- Discuss how a community-based organization engages with local residents to address their concerns and build trust.

- Examine how a government policy change impacts various stakeholders in a specific industry.

Challenges and Strategies for Stakeholder Management:

- Identifying all stakeholders: It’s crucial to comprehensively identify and understand their diverse needs and expectations.

- Balancing competing interests: Different stakeholders may have conflicting priorities, requiring negotiation and compromise.

- Communicating effectively: Clear and transparent communication builds trust and manages stakeholder expectations.

- Engaging stakeholders: Proactive engagement fosters collaboration and addresses concerns before they escalate.

- Measuring impact: Assessing the impact of business activities on various stakeholders helps assess progress and identify areas for improvement.

Conclusion:

Stakeholder management is not a one-time exercise but an ongoing process. By understanding their importance, applying relevant theories and frameworks, and implementing effective strategies, businesses can navigate the complex stakeholder landscape, build trust, and ensure long-term sustainability.

Additionally:

- Consider exploring the concept of corporate social responsibility (CSR) and its connection to stakeholder management.

- Discuss the ethical implications of stakeholder management and the importance of responsible decision-making.

- Research and integrate contemporary examples of businesses successfully engaging with their stakeholders.

3. Political and legal factors affecting business

Introduction:

No business exists in a vacuum. The broader environment, shaped by political and legal forces, significantly impacts how organizations operate, make decisions, and achieve their goals. Understanding these factors is crucial for informed strategic planning, risk management, and navigating the complexities of the external world.

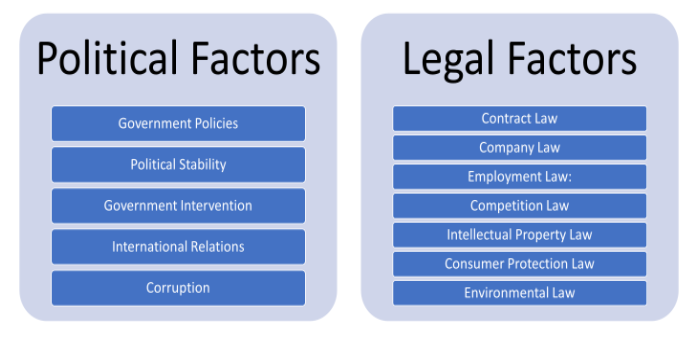

Political Factors:

- Government Policies: Regulations, tax laws, trade agreements, labor laws, environmental regulations, and consumer protection policies all influence business activities and costs.

- Political Stability: Instability, including changes in government, wars, or social unrest, can create uncertainty, disrupt operations, and increase risk.

- Government Intervention: Direct involvement in specific industries (e.g., subsidies, price controls) or economic interventions (e.g., interest rate manipulation) can impact profitability and competition.

- International Relations: Trade policies, sanctions, and political alliances can affect access to markets, resources, and trade partners.

- Corruption: Dishonest practices within government can create unfair competition, increase costs, and hinder business transactions.

Legal Factors:

- Contract Law: Governs agreements between businesses and other parties, outlining rights, obligations, and dispute resolution mechanisms.

- Company Law: Sets rules for company formation, governance, shareholder rights, and reporting requirements.

- Employment Law: Defines minimum wages, working conditions, employee rights, and dismissal procedures.

- Competition Law: Prohibits anti-competitive practices like monopolies and price fixing, ensuring fair competition in the market.

- Intellectual Property Law: Protects patents, trademarks, and copyrights, incentivizing innovation and protecting business assets.

- Consumer Protection Law: Regulates product safety, advertising practices, and consumer rights, ensuring fair treatment and addressing potential harm.

- Environmental Law: Regulates pollution, waste disposal, and resource usage, addressing environmental concerns and ensuring sustainability.

Theories and Illustrations:

- Institutional Theory: Examines how legal and regulatory frameworks shape organizational structures and behaviors, reflecting societal norms and power dynamics.

Adoption of Sustainable Practices: Institutional theory suggests that organizations conform to institutional pressures and norms in their environment. For example, in response to increasing societal concern about environmental sustainability, many businesses have adopted sustainable practices such as reducing carbon emissions, minimizing waste, and implementing eco-friendly production processes. These actions are often driven by the desire to conform to institutional expectations and maintain legitimacy in the eyes of stakeholders.

Corporate Governance Reforms: Institutional theory can also be observed in corporate governance reforms. Following high-profile corporate scandals and financial crises, governments and regulatory bodies often introduce new regulations and standards aimed at improving transparency, accountability, and ethical behavior within organizations. Companies comply with these reforms to conform to institutional norms and avoid reputational damage.

- Transaction Cost Economics: Analyzes the costs associated with different legal structures and regulations, informing decisions about market participation and compliance strategies.

Outsourcing Decisions: Transaction cost economics helps explain decisions related to outsourcing. For example, a manufacturing company may choose to outsource certain production processes to third-party suppliers rather than performing them in-house. This decision is influenced by factors such as the costs of negotiating and enforcing contracts, the uncertainty of future demand, and the availability of specialized expertise. By outsourcing, the company aims to minimize transaction costs and achieve greater efficiency.

Vertical Integration: Transaction cost economics also applies to decisions regarding vertical integration. For instance, a retail company may decide to acquire its suppliers or distributors to streamline operations and reduce transaction costs associated with coordination, quality control, and information asymmetry. Vertical integration allows the company to exert greater control over its supply chain and mitigate the risks of opportunistic behavior by external parties.

- Public Choice Theory: Assumes government policy is influenced by political actors seeking re-election and benefits for their constituents, impacting businesses strategically.

Government Policy Decisions: Public choice theory examines how individuals and groups make decisions within the political system. For example, policymakers may prioritize policies that benefit certain interest groups or constituents, such as tax breaks for specific industries or subsidies for particular agricultural producers. These policy decisions are often influenced by factors such as lobbying efforts, campaign contributions, and electoral incentives.

Voting Behavior: Public choice theory also helps explain voting behavior. Individuals may vote for candidates or parties that promise policies aligned with their own interests or preferences, such as lower taxes, increased social welfare spending, or environmental regulations. Rational self-interest plays a significant role in shaping electoral outcomes and public policy.

Case Studies:

- Analyze how changes in tax laws impact the profitability and investment decisions of businesses in a specific industry.

- Discuss how political instability in a country disrupts supply chains and increases costs for international businesses operating there.

- Examine how antitrust regulations affect competition dynamics and pricing strategies in a specific market.

Challenges and Strategies for Navigating Political and Legal Factors:

- Staying informed: Regular monitoring of political and legal developments is crucial for anticipating changes and adapting strategies.

- Compliance: Ensuring adherence to relevant laws and regulations minimizes legal risks and penalties.

- Advocacy: Engaging with policymakers and advocating for favorable policies can benefit the business and the industry.

- Risk management: Proactive identification and mitigation of potential risks arising from political and legal uncertainties.

- Building relationships: Establishing positive relationships with government officials and regulatory bodies can facilitate communication and smooth operations.

Conclusion:

The political and legal landscape presents both challenges and opportunities for businesses. By understanding these factors, applying relevant theories, and implementing effective strategies, organizations can navigate this complex environment, mitigate risks, and achieve long-term success.

4. Macroeconomic factors

Introduction:

The wider economic environment beyond a specific business plays a crucial role in its performance and decision-making. These macroeconomic factors shape market conditions, consumer behavior, and available resources, influencing profitability, growth, and overall success. Understanding these factors is essential for informed business planning and risk management.

Key Macroeconomic Factors:

- Gross Domestic Product (GDP): Measures the total value of goods and services produced within an economy, indicating its overall size and growth rate. Higher GDP growth generally benefits businesses by increasing demand and consumer spending.

- Inflation: Refers to the sustained increase in the general price level of goods and services, impacting costs and purchasing power. Businesses need to consider inflationary trends when setting prices, planning budgets, and negotiating contracts.

- Interest Rates: Central banks influence the cost of borrowing through interest rates, impacting access to capital for businesses and consumer spending. Rising interest rates can increase borrowing costs for businesses, while decreasing rates can stimulate investment and spending.

- Unemployment Rate: Refers to the percentage of the workforce actively seeking employment but unable to find it. Higher unemployment rates can reduce demand for goods and services, impacting sales and profitability.

- Exchange Rates: Determine the relative value of currencies and influence exports and imports. Businesses involved in international trade need to monitor exchange rate fluctuations to manage costs and optimize pricing.

- Government Debt: Represents the cumulative total of government borrowing, impacting taxes, interest rates, and economic stability. High debt levels can lead to higher taxes or reduced government spending, potentially impacting businesses.

- Consumer Confidence: Reflects consumers’ general optimism about the economy and their future purchasing power. High consumer confidence leads to increased spending, benefiting businesses, while low confidence can dampen demand and economic activity.

Theories and Illustrations:

- Keynesian Economics: Emphasizes government intervention through fiscal policy (spending and taxes) to manage aggregate demand and stimulate economic growth. Businesses need to understand how such policies might impact their markets.

Fiscal Policy during Economic Downturns: Keynesian economics advocates for government intervention in the economy to stimulate demand during times of economic recession. For example, in response to the 2008 financial crisis, governments around the world implemented fiscal stimulus packages consisting of increased government spending and tax cuts to boost consumer and business spending. The rationale behind such measures is to offset the decrease in private sector spending and restore economic growth.

Unemployment Insurance: Keynesian economics supports policies aimed at reducing unemployment during economic downturns. For instance, unemployment insurance programs provide financial assistance to individuals who have lost their jobs, helping to maintain their purchasing power and support aggregate demand in the economy. By providing income support to the unemployed, these programs mitigate the negative effects of recessions on households and help stabilize the economy.

- Monetarism: Focuses on controlling the money supply through monetary policy (interest rates) to achieve economic stability. Businesses need to anticipate the impact of interest rate changes on borrowing costs and investment decisions.

Monetary Policy by Central Banks: Monetarism emphasizes the importance of controlling the money supply to stabilize the economy. For example, central banks such as the Federal Reserve in the United States adjust interest rates and conduct open market operations to influence the money supply and manage inflation. By controlling the supply of money in the economy, central banks aim to maintain price stability and promote sustainable economic growth.

Quantitative Easing (QE):

Monetarist principles have influenced the use of quantitative easing as a monetary policy tool. During the 2008 financial crisis and subsequent economic downturns, central banks engaged in QE programs, whereby they purchased large quantities of government bonds and other securities to inject liquidity into the financial system and stimulate lending and investment. The goal of QE is to lower long-term interest rates, boost asset prices, and support economic activity.

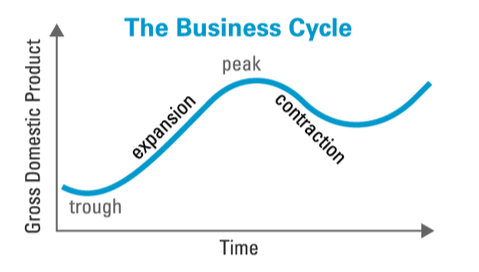

- Business Cycle Theory: Explains the cyclical nature of economic activity with periods of expansion, contraction, and recovery. Businesses need to adapt their strategies based on the current stage of the cycle to optimize performance.

Dot-Com Bubble: Business cycle theory helps explain fluctuations in economic activity over time. For example, during the late 1990s, the rapid growth of internet-related companies led to a speculative bubble known as the dot-com bubble. Stock prices of internet firms soared to unsustainable levels as investors speculated on future profits, fueling a period of economic expansion. However, when the bubble burst in the early 2000s, many internet companies went bankrupt, leading to a recession in the technology sector and a broader economic downturn.

Great Recession: Business cycle theory also helps analyze the causes and consequences of major economic downturns. For instance, the Great Recession of 2008-2009 was triggered by the collapse of the subprime mortgage market in the United States, which led to a financial crisis and a severe contraction in economic activity worldwide. Business cycle theorists study the factors contributing to the onset of recessions, such as asset bubbles, financial imbalances, and external shocks, as well as the mechanisms through which economies recover and return to growth.

Case Studies:

- Analyze how a rise in interest rates impacts borrowing costs and investment decisions for businesses in a specific industry.

- Discuss how fluctuations in exchange rates affect the profitability of export-oriented businesses.

- Examine how changes in government policies, like tax cuts or infrastructure spending, influence aggregate demand and business activity.

Challenges and Strategies for Managing Macroeconomic Factors:

- Uncertainty and volatility: Macroeconomic factors can be unpredictable and subject to sudden changes, requiring businesses to adapt and manage risk.

- Limited control: Businesses cannot directly control these factors, but they can implement strategies to mitigate their impact.

- Strategic planning: Businesses need to consider macroeconomic trends when setting long-term goals, making investments, and allocating resources.

- Diversification: Spreading operations across different markets and product lines can reduce dependence on single economic factors.

- Financial planning: Proactive budgeting and cash flow management help businesses weather periods of economic downturn.

- Monitoring and adaptation: Constant monitoring of macroeconomic developments and adapting strategies accordingly is crucial for success.

Conclusion:

Businesses operate within a dynamic macroeconomic environment. By understanding key factors, applying relevant theories, and implementing effective strategies, organizations can navigate economic challenges, seize opportunities, and achieve sustainable growth.

5. Microeconomic factors

Introduction:

Beyond the broader macroeconomic landscape, businesses operate within a microeconomic environment – a close-up view of the specific market they compete in. Understanding these factors influencing their immediate surroundings is crucial for making informed decisions about pricing, production, marketing, and overall strategy.

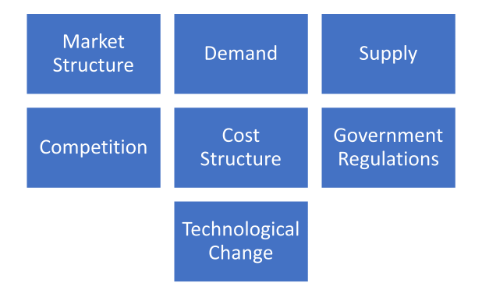

Key Microeconomic Factors:

- Market Structure: Defines the number of buyers and sellers, their relative size, and ease of entry/exit. Common structures include perfect competition which is commonly known for having many buyers and sellers with homogeneous products., monopolistic competition which is known to consist of dominant players, oligopoly, and monopoly. Each affects pricing power, competition intensity, and profit potential.

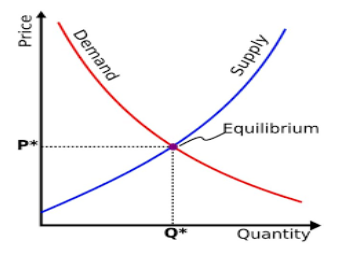

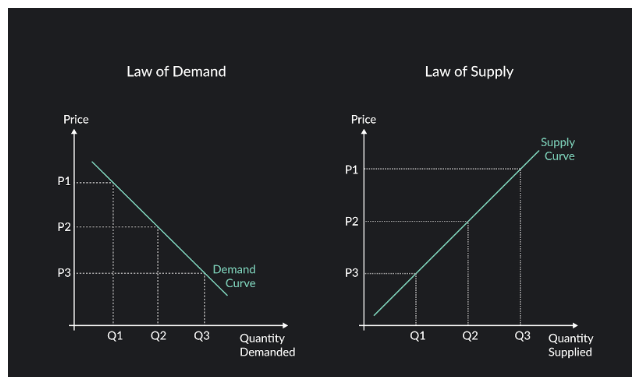

- Demand: Refers to the quantity of a good or service that consumers are willing and able to purchase at different prices. Understanding demand elasticity (responsiveness to price changes) and factors influencing it (consumer income, preferences, substitutes) is vital for setting optimal prices and managing inventory.

- Supply: Refers to the quantity of a good or service that producers are willing and able to offer at different prices. This includes factors like production costs, resource availability, technology, and government regulations. Businesses need to analyze supply-side factors to manage costs and anticipate competitor actions.

- Competition: The presence of other businesses offering similar products or services, influencing market share, pricing strategies, and innovation. Businesses need to analyze competitor strengths, weaknesses, and strategies to gain a competitive edge.

- Cost Structure: Refers to the breakdown of fixed and variable costs associated with producing goods or services. Understanding cost structure helps businesses determine breakeven points, optimize production, and make informed pricing decisions.

- Government Regulations: Specific regulations like price controls, product standards, and environmental restrictions can impact costs, market entry, and business practices. Businesses need to comply with these regulations while advocating for policies that support their long-term goals.

- Technological Change: Continuous advancements in technology can disrupt markets, create new opportunities, and alter production processes. Businesses need to adapt to technological changes to remain competitive and efficient.

Theories and Illustrations:

- Game Theory: Analyzes strategic interactions between competing businesses, helping predict competitor behavior and develop optimal responses.

Oligopoly Competition: Game theory is often used to analyze strategic interactions among competitors in oligopolistic markets. For example, consider the rivalry between two leading smartphone manufacturers. Each company must decide whether to lower its prices to gain market share or maintain higher prices to maximize profits. The decision depends not only on the company’s own actions but also on its expectations of how its competitor will respond. Game theory helps predict outcomes in such scenarios by modeling the strategic choices and potential payoffs of each player.

International Relations and Negotiations: Game theory also applies to international relations and negotiations between countries. For instance, when two countries are engaged in a trade dispute, each must weigh the costs and benefits of imposing tariffs or retaliatory measures. The outcome depends on each country’s perception of its own interests, as well as its expectations of the other country’s actions. Game theory provides a framework for analyzing these interactions and predicting potential outcomes.

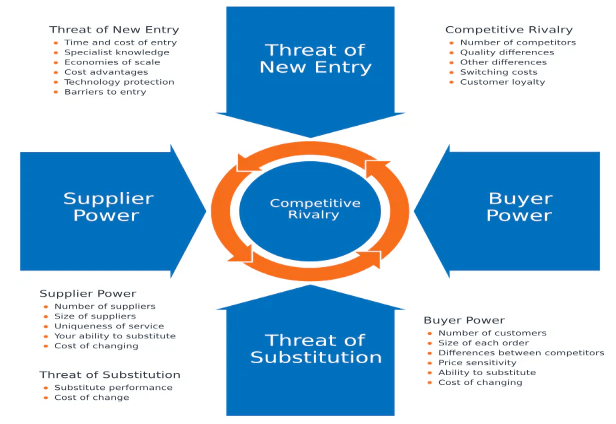

- Porter’s Five Forces: Identifies five key forces shaping competition within an industry: threat of new entrants, bargaining power of buyers, bargaining power of suppliers, threat of substitutes, and competitive rivalry. Businesses can use this framework to assess their competitive landscape and develop strategies.

Airline Industry: Porter’s Five Forces framework can be applied to analyze competition within the airline industry. The threat of new entrants is relatively low due to high capital requirements and regulatory barriers. The bargaining power of suppliers, such as aircraft manufacturers and fuel providers, can impact airline profitability. Additionally, the bargaining power of buyers, including individual passengers and corporate clients, influences ticket prices and service offerings. Competitive rivalry among existing airlines is intense, leading to price wars and efforts to differentiate through amenities or loyalty programs. Lastly, the threat of substitutes, such as trains or cars for short-haul travel, affects demand and pricing strategies.

Retail Industry: In the retail industry, Porter’s Five Forces can help analyze the competitive dynamics. The threat of new entrants is moderate, with barriers such as economies of scale, brand loyalty, and distribution networks. Suppliers wield varying degrees of bargaining power, depending on factors like product differentiation and availability of alternative sources. Retailers must also contend with the bargaining power of buyers, who can demand lower prices or higher quality products. Intense rivalry among existing competitors often leads to price competition and promotional strategies. Finally, the availability of substitutes, such as online shopping or alternative retail formats, shapes consumer preferences and purchasing behavior.

- Price Theory: Explains the relationship between price and demand, offering frameworks like elastic vs. inelastic demand and marginal cost pricing to help businesses optimize pricing strategies.

Consumer Demand: Price theory helps explain consumer behavior in response to changes in prices. For example, if the price of gasoline rises, consumers may reduce their driving habits or seek alternative modes of transportation. Conversely, if the price of a particular smartphone decreases, consumers may be more inclined to purchase it.

Producer Decisions: Price theory also influences producer decisions regarding pricing strategies and production levels. For instance, a company may adjust its pricing based on market demand and competitor pricing to maximize revenue. Additionally, price theory guides decisions about production levels, where firms aim to produce the quantity that maximizes profit given cost considerations and market demand.

Case Studies:

- Analyze how a change in government regulations affecting a specific industry impacts competition and pricing strategies within that industry.

- Discuss how a technological innovation disrupts an existing market and creates opportunities for new entrants or forces incumbents to adapt.

- Examine how a business leverages its understanding of competitor strengths and weaknesses to gain market share in a highly competitive landscape.

Challenges and Strategies for Managing Microeconomic Factors:

- Complexity and dynamism: Microeconomic factors constantly evolve, requiring ongoing monitoring and adaptation.

- Limited control: Businesses cannot directly control these factors, but they can implement strategies to mitigate their impact and capitalize on opportunities.

- Market research and analysis: Regularly gathering and analyzing market data is crucial for understanding demand, competition, and trends.

- Innovation and differentiation: Developing unique products, services, or processes can help businesses stand out from competitors.

- Cost management: Optimizing production processes, negotiating with suppliers, and controlling expenses are essential for profitability.

- Strategic partnerships: Collaborating with other businesses can offer advantages like sharing resources, entering new markets, or developing complementary products.

Conclusion:

Businesses navigating the microeconomic environment require a keen understanding of the market they operate in and the factors influencing it. By applying relevant theories, conducting thorough analysis, and implementing effective strategies, businesses can adapt to changing circumstances, gain a competitive edge, and achieve sustainable success.

6. Social and demographic factors

Introduction:

Beyond economic forces, businesses operate within a dynamic social and demographic landscape. Understanding these factors, the values, attitudes, and characteristics of the population, is crucial for informed decision-making about products, marketing, branding, and overall strategy. By aligning with or responding to social and demographic trends, businesses can gain a competitive edge and contribute to positive societal impact.

Key Social and Demographic Factors:

- Consumer Values and Lifestyles: Shifting societal values around sustainability, health, ethical practices, and work-life balance influence consumer preferences and purchasing decisions. Businesses need to understand these evolving values and adapt their offerings and messaging accordingly.

- Demographics: Factors like age, gender, income, education level, ethnicity, and family structure influence consumption patterns and market potential. Businesses need to analyze their target demographics and adjust their strategies to reach the right audience effectively.

- Social Media and Technology: The rise of social media and digital communication platforms has changed how consumers connect with brands and access information. Businesses need to leverage these platforms effectively for marketing, engagement, and building brand communities.

- Urbanization and Globalization: Increased urbanization and global interconnectedness create diverse markets with unique needs and preferences. Businesses need to consider cultural nuances and adapt their offerings to resonate with different audiences.

- Education and Skills: The changing nature of work and evolving skill requirements impact the talent pool available to businesses. Businesses need to invest in workforce development and adapt their recruitment strategies to attract and retain skilled professionals.

- Environmental Attitudes and Regulations: Growing concerns about climate change and environmental sustainability influence consumer behavior and government regulations. Businesses need to adopt sustainable practices and communicate their environmental commitment to gain public trust and comply with regulations.

- Geopolitical Landscape: Political instability, social unrest, and international conflicts can disrupt supply chains, affect consumer confidence, and create risks for businesses operating globally. Businesses need to monitor geopolitical developments and adjust their strategies accordingly.

Theories and Illustrations:

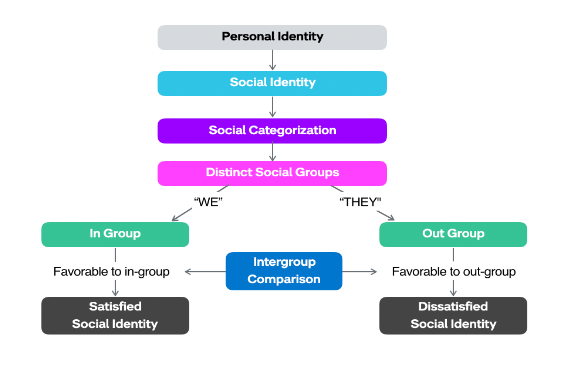

- Social Identity Theory: Explains how individuals identify with social groups and how these identities influence their values, preferences, and purchasing decisions. Businesses can use this theory to understand their target audience and tailor messaging accordingly.

Sports Fandom: Social identity theory can be observed in sports fandom, where individuals identify themselves with a particular sports team. For example, fans of a soccer team may develop a strong sense of belonging and loyalty to their team, viewing it as an extension of their own identity. They may exhibit ingroup favoritism, supporting their team while showing bias against rival teams. This identification with the team contributes to a sense of community among fans and shapes their behaviors, such as attending games, purchasing team merchandise, and engaging in discussions with other fans.

Religious Groups: Social identity theory is also evident in religious groups, where individuals identify with a specific religious denomination or faith tradition. For instance, members of a particular religious community may share common beliefs, values, and rituals that differentiate them from members of other religious groups. Their identification with the religious group influences their sense of belonging, social interactions, and adherence to religious practices.

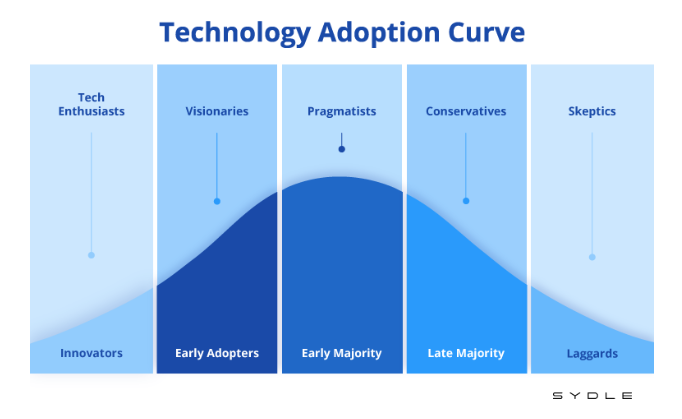

- Diffusion of Innovations Theory: Explains how new ideas and technologies spread through a population over time. Businesses can use this theory to understand how to launch and market new products effectively.

Adoption of Electric Vehicles: Diffusion of innovations theory helps explain the spread of new technologies through society. For example, the adoption of electric vehicles (EVs) has followed a diffusion curve, starting with innovators and early adopters before gradually reaching the mainstream market. Early adopters of EVs were often environmentally conscious consumers or technology enthusiasts who were willing to pay a premium for the latest innovations. As EV technology matured and prices declined, the technology diffused to a wider audience, including mainstream consumers who were attracted by factors such as cost savings on fuel and government incentives.

Spread of Social Media Platforms: The diffusion of innovations theory can also be applied to the spread of social media platforms. For instance, platforms like Facebook, Twitter, and Instagram began as niche services targeting specific user groups, such as college students or photography enthusiasts. Over time, these platforms gained traction among early adopters and influencers, leading to rapid growth in user adoption. As social media became more integrated into daily life and communication practices, it diffused across diverse demographic groups and geographical regions.

- Stakeholder Theory: Argues that businesses should consider the interests of all stakeholders, including society and the environment, beyond just shareholders. This theory can guide businesses towards responsible and sustainable practices.

Corporate Social Responsibility (CSR): Stakeholder theory emphasizes the importance of considering the interests of all stakeholders affected by a company’s actions. For example, a multinational corporation may implement CSR initiatives to address the concerns of various stakeholders, including employees, customers, communities, and investors. These initiatives could involve environmental sustainability programs, employee welfare initiatives, philanthropic activities, and ethical business practices.

Supply Chain Management: Stakeholder theory also informs practices in supply chain management, where companies seek to balance the interests of suppliers, manufacturers, distributors, and customers. For instance, a company may collaborate with its suppliers to ensure fair labor practices, environmental sustainability, and product quality throughout the supply chain. By treating suppliers as valued stakeholders, the company aims to build long-term relationships based on trust, mutual benefit, and shared values.

Case Studies:

- Analyze how a clothing brand adapts its messaging and product offerings to resonate with diverse demographic groups across different countries.

- Discuss how a technology company leverages social media platforms to build a community and engage with its customers directly.

- Examine how a food company integrates sustainable practices into its operations and communicates its environmental commitment to gain consumer trust.

Challenges and Strategies for Managing Social and Demographic Factors:

- Complexity and dynamism: Social and demographic factors are constantly evolving, requiring continuous monitoring and adaptation.

- Diversity and cultural nuances: Understanding and catering to diverse markets with different values and preferences can be challenging.

- Ethical considerations: Balancing business interests with social responsibility and environmental sustainability requires careful consideration and ethical decision-making.

- Market research and analysis: Regularly conducting market research and analyzing demographic trends is crucial for understanding customer needs and preferences.

- Innovation and agility: Adapting offerings and business models to respond to changing needs and opportunities is essential for staying competitive.

- Building relationships and trust: Engaging with stakeholders, including communities and influencers, fosters understanding and builds trust, strengthening social impact.

Conclusion:

Businesses that understand and actively engage with social and demographic factors can thrive in a dynamic and evolving environment. By applying relevant theories, conducting thorough research, and implementing responsible strategies, businesses can contribute to a positive social impact while achieving sustainable success.

7. Technological factors

Introduction:

In today’s rapidly evolving world, technology plays a transformative role in every aspect of business. Understanding these technological factors and their impact is crucial for organizations to adapt, innovate, and thrive in the digital age. This in-depth exploration delves into key technological factors, explores relevant theories, and provides case studies and strategies for navigation.

Key Technological Factors:

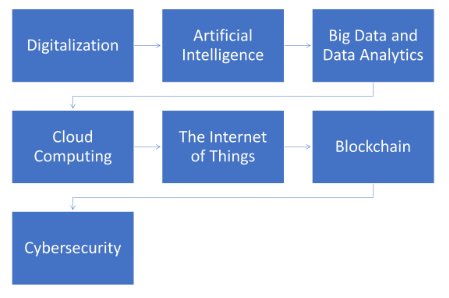

- Digitalization: The conversion of analog information and processes into digital formats, enabling automation, data analysis, and online interactions. This impacts nearly every aspect of business, from marketing and communication to production and delivery.

- Artificial Intelligence (AI) and Machine Learning (ML): Algorithms capable of learning, adapting, and making decisions, automating tasks, improving efficiency, and driving insights. These technologies can personalize customer experiences, optimize operations, and uncover hidden patterns in data.

- Big Data and Data Analytics: Collecting, storing, and analyzing vast amounts of data to extract valuable insights, inform decision-making, and predict future trends. This empowers businesses to understand customer behavior, target marketing efforts effectively, and identify potential risks and opportunities.

- Cloud Computing: Delivering on-demand access to computing resources like servers, storage, and software over the internet, offering scalability, flexibility, and cost-efficiency. This allows businesses to scale resources up or down as needed and avoid maintaining expensive physical infrastructure.

- The Internet of Things (IoT): Interconnected devices with sensors and internet connectivity, collecting and sharing data, enabling automation and remote monitoring. This can be used in various applications, from smart homes and wearables to connected factories and supply chains.

- Blockchain: A distributed ledger technology ensuring secure and transparent data sharing, fostering trust and streamlining processes. This has potential applications in areas like financial transactions, supply chain management, and intellectual property protection.

- Cybersecurity: Protecting data and systems from unauthorized access, use, disclosure, disruption, modification, or destruction. As technology advances, so do cyber threats, making cybersecurity a critical concern for businesses of all sizes.

Theories and Illustrations:

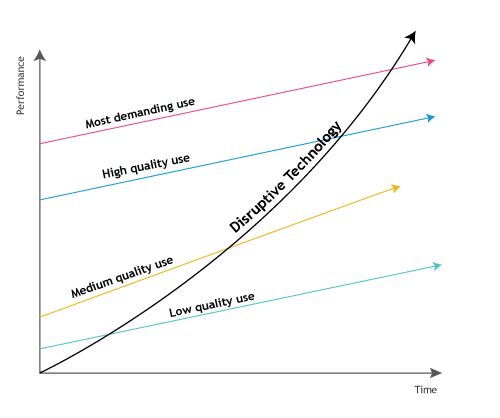

- Disruption Theory: Explains how new technologies can rapidly render existing business models obsolete, requiring adaptation and innovation to survive. Businesses need to be aware of potential disruptions and prepare for them.

- Diffusion of Innovations Theory: Explains how new ideas and technologies spread through a population over time. Understanding the stages of this diffusion helps businesses develop effective marketing and adoption strategies.

- Transaction Cost Economics: Analyzes the costs associated with different organizational structures and technologies, helping businesses choose the most efficient option for their operations.

Case Studies:

- Analyze how a music streaming service uses AI and big data to personalize recommendations and improve user experience.

- Discuss how a manufacturing company leverages the IoT to monitor production processes and optimize efficiency.

- Examine how a financial institution uses blockchain technology to facilitate secure and transparent cross-border transactions.

Challenges and Strategies for Managing Technological Factors:

- Rapid change and uncertainty: Keeping pace with rapid technological advancements and anticipating future trends can be challenging.

- Cost and investment: Implementing new technologies can require significant investments in infrastructure, training, and ongoing maintenance.

- Integration and security: Integrating new technologies seamlessly with existing systems while ensuring data security is crucial.

- Ethical considerations: The use of new technologies raises ethical issues around privacy, security, and job displacement. Businesses need to address these concerns responsibly.

- Embrace learning and adaptation: Fostering a culture of continuous learning and encouraging employee adaptation to technological changes is essential.

- Invest in R&D and innovation: Staying ahead of the curve requires ongoing investment in research and development to explore new technologies and identify potential applications.

- Collaborate with technology partners: Partnering with technology companies can provide access to expertise and resources, enabling faster adoption and integration of new technologies.

- Focus on value creation: Clearly understand how new technologies can create value for the business and its stakeholders before investing.

Conclusion:

Technological factors are a driving force shaping the business landscape. By understanding these factors, applying relevant theories, and implementing effective strategies, businesses can harness the power of technology to enhance competitiveness, create new opportunities, and achieve sustainable success.

Additionally:

- Consider delving into the ethical implications of technological advancements, such as automation and artificial intelligence.

- Explore the role of technology in addressing global challenges, such as climate change and resource scarcity.

- Investigate the impact of technology on specific industries, such as retail, healthcare, and finance.

- Research successful examples of businesses leveraging technology to overcome challenges and achieve remarkable results.

By continuously learning and adapting, businesses can thrive in the ever-evolving technological landscape, ensuring their relevance and success in the digital landscape.

8. Environmental and sustainability factors

Introduction:

The environment is no longer just a backdrop for business; it’s a critical influencer and increasingly, a factor defining success. Understanding environmental and sustainability factors is essential for navigating a changing world and ensuring long-term organizational viability. This in-depth exploration delves into key issues, relevant theories, and strategies for navigating this complex landscape.

Key Environmental and Sustainability Factors:

- Climate Change: Rising global temperatures, extreme weather events, and sea level rise pose significant risks to businesses, disrupting supply chains, impacting resources, and damaging infrastructure. Businesses need to adapt their operations and mitigate their own emissions.

- Resource Scarcity: Limited availability of resources like water, energy, and raw materials presents both challenges and opportunities. Businesses need to adopt resource-efficient practices and explore alternatives.

- Biodiversity Loss: The decline of ecosystems and species threatens natural resources and poses economic risks. Businesses need to integrate biodiversity considerations into their operations and support conservation efforts.

- Pollution: Air, water, and soil pollution have negative impacts on human health and the environment, leading to regulations and reputational risks. Businesses need to minimize their pollution footprint and invest in clean technologies.

- Social Responsibility and Stakeholder Expectations: Consumers, investors, and other stakeholders increasingly demand environmental and social responsibility from businesses. Businesses need to demonstrate their commitment to sustainability through transparent reporting and responsible practices.

- Circular Economy: Transitioning from a linear “take-make-dispose” model to a circular economy, where resources are kept in use for as long as possible, minimizes waste and creates new opportunities. Businesses need to explore circular economy principles in their design, production, and consumption models.

- Regulations and Policy: Governments are implementing stricter environmental regulations and policies, impacting business operations and costs. Businesses need to comply with these regulations and advocate for policies that support sustainable development.

Theories and Illustrations:

- Natural Resource Theory: Explains how limited natural resources can constrain economic growth and highlights the need for efficient resource use. Businesses can utilize this theory to identify risks and opportunities associated with resource scarcity.

- Stakeholder Theory: Argues that businesses should consider the interests of all stakeholders, including the environment and future generations. This theory emphasizes the importance of environmental responsibility and long-term sustainability.

- Porter’s Five Forces: Can be adapted to analyze the environmental context of an industry, considering the threat of new entrants, bargaining power of buyers and suppliers, and competitive rivalry within the context of shared environmental challenges and regulations.

Case Studies:

- Analyze how a fashion brand implements circular economy principles by designing clothes for disassembly and utilizing recycled materials.

- Discuss how a tech company tackles climate change by investing in renewable energy and carbon offsetting projects.

- Examine how a food company reduces its water footprint through resource-efficient irrigation techniques and partnerships with local farmers.

Challenges and Strategies for Managing Environmental and Sustainability Factors:

- Complexity and uncertainty: The environmental landscape is complex and constantly evolving, requiring ongoing monitoring and adaptation.

- Costs and investments: Implementing sustainable practices often requires upfront investments in new technologies and processes.

- Balancing competing priorities: Short-term financial goals may conflict with long-term sustainability objectives.

- Transparency and communication: Building trust and engaging stakeholders requires transparent reporting and communication of environmental performance.

- Collaboration and partnerships: Working with governments, NGOs, and other businesses can accelerate progress towards sustainability goals.

- Innovation and new technologies: Exploring and investing in innovative solutions like renewable energy, resource-efficient technologies, and circular economy models is crucial.

- Life Cycle Assessment: Evaluating the environmental impact of products and services throughout their entire life cycle helps identify hotspots and prioritize improvement efforts.

Conclusion:

Businesses that integrate environmental and sustainability factors into their core strategies are not only mitigating risks but also unlocking new opportunities and gaining a competitive edge. By understanding these factors, applying relevant theories, and implementing effective strategies, businesses can contribute to a sustainable future and achieve long-term success.

9. Competitive factors

Understanding the competitive landscape is crucial for any business seeking success. In this chapter, we’ll delve deeply into the various factors that define competition, explore relevant theories, and provide illustrations and strategies for navigating this dynamic environment.

Key Competitive Factors:

- Market Structure: Different market structures, like perfect competition, oligopoly, and monopoly, influence the intensity of competition, pricing power, and potential profitability. Identifying your market structure helps you understand the game you’re playing.

- Number of Competitors: The number of players in the market directly impacts competition. With numerous competitors, differentiation and strategic marketing become critical.

- Competitor Strengths and Weaknesses: Analyzing your competitors’ capabilities, resources, and strategies helps you identify competitive threats and opportunities to exploit their weaknesses.

- Threat of New Entrants: Factors like barriers to entry, brand loyalty, and regulatory hurdles determine the ease of new businesses entering the market. Managing entry barriers and innovating continuously are crucial.

- Bargaining Power of Buyers and Suppliers: The negotiating power of buyers and suppliers can significantly impact your profitability. Building strong relationships and exploring alternative options are essential.

- Substitute Products and Services: Identifying and understanding substitute offerings from alternative industries or technologies helps you stay ahead of potential disrupters.

- Price Sensitivity of Customers: The degree to which customers are price-sensitive influences pricing strategies. Understanding customer value perceptions and offering differentiated value propositions is key.

- Technology and Innovation: Rapid technological advancements can change the competitive landscape quickly. Embracing innovation, adapting to new technologies, and staying ahead of the curve are vital.

- Regulatory Environment: Government regulations and policies can impact competition by influencing market access, product standards, and pricing mechanisms. Staying informed and advocating for favorable policies is crucial.

Theories and Illustrations:

- Game Theory: Analyzes strategic interactions between competitors, helping predict competitor behavior and develop optimal responses. Imagine a pricing war as a game, where choosing the right strategy depends on competitor moves.

- Porter’s Five Forces: This framework identifies five key forces shaping competition within an industry (threat of new entrants, bargaining power of buyers, bargaining power of suppliers, threat of substitutes, and competitive rivalry). Analyzing these forces helps you understand your competitive landscape and develop strategies.

- Resource-Based View: This theory posits that a firm’s unique resources and capabilities are the source of its competitive advantage. Identifying and leveraging your unique strengths are crucial to stand out in the market.

Case Studies:

- Analyze how Uber disrupted the taxi industry by leveraging technology and a different market structure.

- Discuss how Apple maintains its competitive edge in the smartphone market through unique product design, brand loyalty, and a closed ecosystem.

- Examine how Amazon navigates the intense competition in online retail by offering diverse product categories, competitive pricing, and excellent customer service.

Challenges and Strategies for Managing Competitive Factors:

- Dynamic and evolving: The competitive landscape constantly changes, requiring continuous monitoring and adaptation.

- Limited resources: Balancing investments in various aspects while staying competitive can be challenging.

- Uncertainty and predicting competitor actions: Accurately anticipating competitor moves and market trends can be difficult.

- Maintaining a competitive advantage: Sustaining differentiation in a dynamic market requires ongoing innovation and strategic focus.

- Market research and competitor analysis: Regularly gathering and analyzing market data and competitor information is crucial for informed decision-making.

- Developing a competitive strategy: Formulating a clear strategy based on your strengths, weaknesses, and the competitive landscape guides your actions.

- Innovation and differentiation: Offering unique value propositions and continuously innovating helps you stand out from the crowd.

- Collaboration and partnerships: Strategic partnerships can access new resources, expand reach, and gain competitive advantages.

- Building strong relationships: Fostering positive relationships with key stakeholders, including customers and suppliers, strengthens your competitive position.

Conclusion:

Competing effectively requires a deep understanding of the competitive landscape, your place within it, and the ability to adapt to dynamic changes. By applying relevant theories, conducting thorough analysis, and implementing effective strategies, businesses can gain a competitive edge and achieve sustainable success.