F2 – Chapter 1- The Nature, Source, and Purpose of Management Information

Topic 1: Accounting for management

In the dynamic business landscape, navigating the complexities of managerial decision-making requires reliable and insightful information. This in-depth exploration delves into the purpose and role of management accounting, its distinction from financial accounting, and its crucial contribution to planning, control, and informed decision-making, while acknowledging its inherent limitations.

A. Unveiling the Power of Cost and Management Accounting:

- Purpose: Provides detailed information about an organization’s costs, activities, and performance, supporting decision-making, planning, and control beyond financial reporting.

- Role:

- Cost analysis: Identifies, measures, and analyzes costs associated with products, services, departments, and activities.

- Performance evaluation: Assesses and measures the effectiveness and efficiency of operations.

- Planning and budgeting: Formulates budgets, forecasts future performance, and supports strategic decision-making.

- Control and profitability improvement: Identifies areas for cost reduction and performance improvement.

Illustration: A manufacturing company utilizes cost accounting to determine product profitability, identify cost-saving opportunities, and develop budgets for future production, optimizing resource allocation and maximizing profitability.

B. Contrasting Financial and Management Accounting:

| Feature | Financial Accounting | Management Accounting |

| Primary users | External stakeholders (investors, creditors, regulators) | Internal managers |

| Focus | Historical financial performance | Future performance and decision-making |

| Regulations | Adheres to strict accounting standards | Adaptable to specific organizational needs |

| Level of detail | Aggregated financial statements | Detailed cost and activity data |

| Reporting frequency | Periodic (quarterly, annually) | Continuous and flexible |

C. Navigating the Planning, Decision-Making, and Control Cycle:

I) Planning: Management accounting facilitates setting strategic, tactical, and operational goals by:

- Strategic planning: Analyzing long-term trends, competitor analysis, and market potential to define overall direction.

- Tactical planning: Budgeting resource allocation for specific departments or projects to achieve strategic goals.

- Operational planning: Establishing detailed plans for day-to-day activities and resource utilization.

II) Decision-Making: Cost and performance information empowers managers to:

-

- Identify profitable products and services: Allocate resources strategically based on profitability analysis.

- Evaluate investment opportunities: Assess capital budgeting proposals based on projected costs and financial returns.

- Set effective pricing strategies: Analyze cost structures and competitor pricing to optimize pricing decisions.

III) Control: Management accounting enables monitoring and adjusting plans by:

-

- Comparing actual performance to budget: Identify variances and investigate potential problems.

- Taking corrective actions: Implement measures to address deviations and control costs.

- Evaluating operational efficiency: Analyze performance metrics to identify areas for improvement.

Illustration: A retail chain utilizes cost accounting to identify underperforming product lines, adjust pricing strategies, and implement cost-saving measures, improving overall profitability and control over operations.

D. Differentiating Planning Horizons:

- Strategic planning: Long-term (3-5 years), focuses on overall business direction and competitive advantage.

- Tactical planning: Mid-term (1-3 years), translates strategic goals into specific objectives and resource allocation plans.

- Operational planning: Short-term (days, weeks, months), defines detailed execution plans for day-to-day activities.

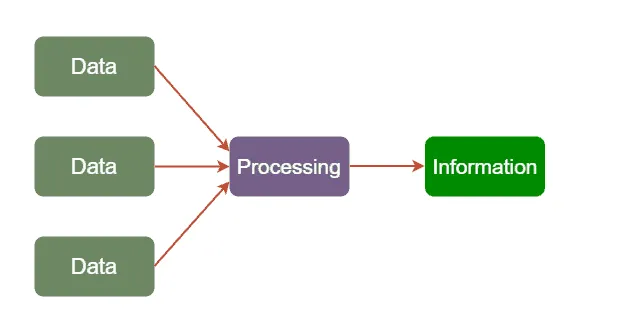

E. Data vs. Information: Recognizing the Distinction:

- Data: Raw, unprocessed facts and figures.

- Information: Data that has been processed, formatted, and presented in a meaningful way, providing context and value to users.

Illustration: Sales figures (data) become valuable information when analyzed by product category, customer segment, and profitability, providing insights for sales strategy and resource allocation

F. Hallmarks of Good Management Information:

- Accurate: Free from errors and reflects the true state of affairs.

- Relevant: Addresses the specific needs and questions of the user.

- Complete: Provides all the necessary information to make informed decisions.

- Timely: Available when needed for decision-making.

- Understandable: Presented in a clear and concise format that users can easily comprehend.

G. Acknowledging the Limitations of Management Information:

- Uncertainty: Future events may not unfold as predicted, and information may become outdated.

- Subjectivity: Judgments and assumptions used in gathering or interpreting data can introduce bias.

- Incomplete: No information system can capture all relevant factors impacting decision-making.

Illustration: A cost analysis may not fully capture the qualitative aspects of customer preferences, potentially leading to suboptimal decisions if over-relying on purely cost-based information.

Topic 2. Sources of data

In the dynamic world of business, management accounting relies heavily on accurate and relevant information to fuel informed decision-making. This in-depth exploration delves into the diverse sources of data available, both internal and external, and examines their uses, limitations, and cost considerations

A. Unveiling the Three Main Data Sources:

-

Machine/Sensor Data:

- Description: Continuous data generated by machines, sensors, and automated systems (e.g., production output, equipment performance, energy consumption).

- Uses: Real-time monitoring, performance evaluation, predictive maintenance, process optimization.

- Limitations: Requires data security measures, potential integration challenges with existing systems, data overload.

- Illustration: A manufacturing plant uses sensor data to monitor machine performance, predict potential failures, and schedule preventive maintenance, reducing downtime and production costs.

-

Transactional Data:

- Description: Data generated from business transactions (e.g., sales invoices, purchase orders, payroll records, expenses).

- Uses: Financial reporting, cost analysis, profitability assessment, inventory management.

- Limitations: Accuracy depends on data entry quality, may require cleansing and standardization for further analysis.

- Illustration: A retail store analyzes sales transaction data to identify best-selling products, optimize pricing strategies, and manage inventory levels, maximizing sales and profitabilit

-

Human/Social Data:

- Description: Information gathered from human interaction and engagement (e.g., surveys, customer feedback, employee reports, social media sentiment analysis).

- Uses: Market research, customer satisfaction assessment, employee engagement evaluation, brand reputation monitoring.

- Limitations: Subjectivity of responses, potential sampling bias, ethical considerations for data collection and usage.

- Illustration: A company conducts employee surveys to gauge morale, identify areas for improvement, and implement programs to enhance employee engagement, leading to improved productivity and reduced turnover.

B. Exploring Internal/ External Information Sources v Primary and Secondary Sources:

-

Internal Sources:

- Accounting records: General ledger, sub-ledgers, budgets, forecasts, cost reports.

- Sales & marketing data: Customer relationship management (CRM) systems, sales records, customer feedback.

- Operations data: Production records, inventory levels, machine performance data.

- Human resources data: Payroll records, employee performance evaluations, training records.

-

External Sources:

- Government statistics: Industry reports, economic data, demographic information.

- Financial press: Business news, company reports, analyst commentaries.

- Professional/trade associations: Industry benchmarks, research reports, best practices guides.

- Quotations and price lists: Supplier catalogs, industry databases, online marketplaces.

Primary vs Secondary Sources

I) Primary Sources

Definition: Original data collected firsthand for a specific purpose

Examples:

- Surveys and questionnaires

- Interviews with customers/staff

- Direct observations

- Internal company records (sales data, timesheets)

- Experiments and tests

Advantages: Tailored to your needs, current, exclusive Disadvantages: Time-consuming, expensive to collect

II) Secondary Sources

Definition: Data already collected by others for different purposes

Examples:

- Government statistics

- Industry reports

- Published research

- Competitor websites

- Trade journals and newspapers

Advantages: Quick, cheap, readily available Disadvantages: May be outdated, not specific to your needs, available to competitors

C. Using Published Information Wisely:

Uses:

- Benchmarking: Compare own performance with industry averages.

- Market research: Understand market trends, competitor analysis, identify new opportunities.

- Investment decisions: Analyze financial reports, evaluate company performance.

- Stay informed: Keep up with industry news, regulatory changes, emerging trends.

Limitations:

- Accuracy: Verify information source and credibility, be cautious of biased reporting.

- Relevance: Ensure information is applicable to your specific industry and context.

- Timeliness: Information may be outdated, consider publication date and potential changes.

- Accessibility: Some information may require subscriptions or fees for access.

Illustration: A startup company utilizes industry reports from a trade association to understand market size, customer preferences, and competitor offerings, informing their product development and market entry strategy.

D. Data Capture Costs of Management Accounting Information:

Definition

Data capture costs = costs incurred in collecting, recording, and processing information for management accounting purposes

Types of Data Capture Costs

- Direct Costs

- Salaries of data entry staff

- Cost of data collection forms/software

- Equipment costs (scanners, computers)

- Storage costs (servers, cloud storage)

- Training costs for data handlers

- Indirect Costs

- Time spent by operational staff recording data

- System maintenance and updates

- Data verification and quality checks

- Lost productivity during data collection

Key Considerations

Cost vs Benefit Analysis

Information should only be collected if:

- Benefits > Costs

- The information improves decision-making

- It provides competitive advantage

- It’s required by law/regulation

Factors Affecting Data Capture Costs

Higher costs when:

- Primary sources used (vs secondary)

- Manual data entry (vs automated)

- High accuracy requirements

- Real-time data needed

- Large data volumes

- Complex data formats

Lower costs when:

- Automated systems in place

- Integrated IT systems

- Secondary sources available

- Simple, standardized formats

Cost Reduction Strategies

- Automate data capture (barcode scanners, RFID)

- Integrate systems to avoid duplicate entry

- Standardize data formats across organization

- Use exception reporting (only capture unusual items)

- Sampling instead of 100% data collection

Topic 3. Cost classification

In the intricate world of management accounting, understanding cost classifications and behaviors is fundamental to informed decision-making. This in-depth exploration delves into the distinction between production and non-production costs, delves into various cost elements, highlights their importance in valuing output and inventories, and explains additional cost classifications for insightful analysis.

A. Production vs. Non-Production Costs:

Production Costs: Costs directly involved in manufacturing products or providing services.

- Illustration: Raw materials used in a product, direct labor costs for manufacturing, energy consumed during production.

Non-Production Costs: Costs not directly involved in production but necessary for running the business.

- Illustration: Rental expenses for office space, marketing and advertising costs, salaries of administrative staff.

Distinguishing between these is crucial for:

- Inventory valuation: Only production costs are capitalized and included in the cost of inventory.

- Profitability analysis: Understanding how each cost impacts overall profit margin.

- Decision-making: Identifying cost-saving opportunities in specific areas.

B. Unveiling the Non-Production Cost Elements:

- Administrative Costs: Expenses related to general management and organization of the business.

- Examples: Salaries of administrative staff, accounting fees, legal fees.

- Selling Costs: Expenses incurred to promote and sell products or services.

- Examples: Advertising costs, sales commissions, salaries of sales staff.

- Distribution Costs: Expenses associated with delivering products or services to customers.

- Examples: Transportation costs, warehousing costs, customer service costs.

- Finance Costs: Expenses related to borrowing money and managing finances.

- Examples: Interest on loans, bank charges, foreign exchange losses.

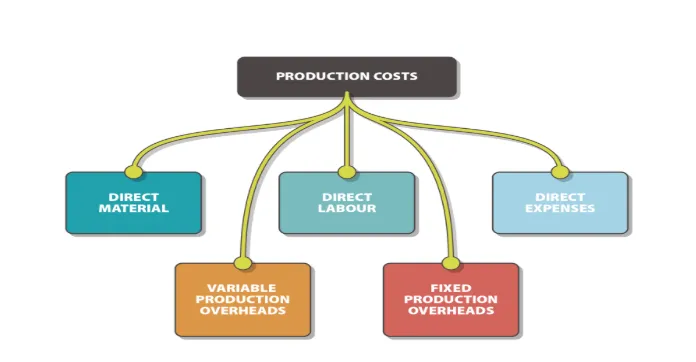

C. Decoding Production Cost Elements:

- Direct Materials: Materials directly identifiable with a specific product or service.

- Illustration: Fabric used in a garment, wood used in furniture.

- Direct Labor: Wages paid to employees directly involved in production.

- Illustration: Wages of assembly line workers, salaries of surgeons.

- Overheads (Indirect Costs): Production costs not directly attributable to a specific product or service, allocated using various methods.

- Examples: Factory rent, electricity costs, depreciation of production equipment.

D. Valuing Inventory and Profits:

- Only production costs (materials, labor, overheads) are included in the cost of inventory.

- Non-production costs are expensed in the period they are incurred, affecting the current period’s profit.

- Understanding this distinction ensures accurate inventory valuation and reflects true profitability.

E. Exploring Additional Cost Classifications:

- By Function: Classifies costs according to their business function (e.g., production, marketing, administration).

- Direct vs. Indirect: Direct costs are traceable to specific cost objects (products, services), while indirect costs are allocated using various methods.

- Fixed vs. Variable: Fixed costs remain constant regardless of activity level, while variable costs change with activity level.

- Stepped Fixed Costs: Change in fixed cost amounts only at specific activity levels.

- Semi-Variable Costs: Have both fixed and variable components.

Illustration: Rent is a fixed cost, while direct labor is a variable cost. Electricity might be a stepped fixed cost, changing at specific usage levels.

F. Categorizing Transactions with Codes:

- Unique codes assigned to different cost categories ensure accurate data capture and analysis.

- These codes facilitate filtering and reporting based on specific cost elements or classifications.

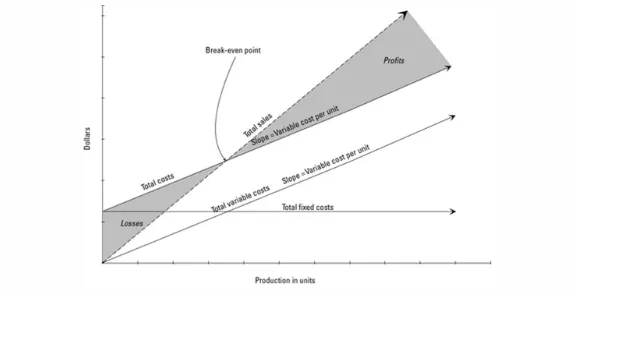

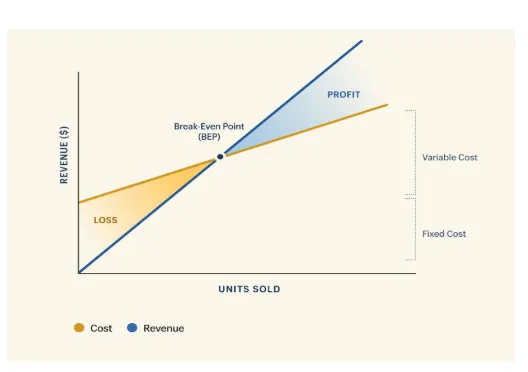

G. Visualizing Cost Behavior:

- Cost behavior can be illustrated using graphs like scatter plots, cost-volume-profit (CVP) charts, and break-even charts.

Cost-volume-profit Chart

Break-even chart

- These visual representations help understand how costs change with activity levels and make informed pricing and production decisions.

H. Cost Objects, Units, and Centers:

- Cost object: Anything for which costs are accumulated (e.g., product, service, project).

- Cost unit: The unit of measurement used to express the cost of a cost object (e.g., per unit, per hour).

- Cost center: A department or area where costs are incurred and monitored (e.g., production department, marketing department).

I. Profit vs. Cost vs. Investment vs. Revenue Centers:

- Cost center: Incurred costs (e.g., production department).

- Profit center: Generates revenue and incurs costs, measured by profit (e.g., sales department).

- Investment center: Focuses on long-term investments and returns (e.g., research and development department).

- Revenue center: Generates revenue but may not incur significant costs

J. Information Needs for Different Center Managers:

- Cost center managers: Focus on controlling and minimizing costs within their department. Need information on cost variances, resource utilization, and efficiency metrics.

- Profit center managers: Responsible for both revenue generation and cost control. Need information on sales volume, profitability by product or service, and marketing effectiveness.

- Investment center managers: Evaluate long-term investments and returns. Need information on project profitability, return on investment (ROI), and risk assessments.

- Revenue center managers: Primarily concerned with generating revenue. Need information on customer segments, sales performance, and marketing campaign effectiveness.

Topic 4. Presenting information

In the dynamic world of business, presenting management information in a clear, concise, and insightful manner is crucial for informed decision-making. This in-depth exploration delves into crafting impactful written reports and utilizing data visualization techniques to transform data into meaningful understanding.

A. Tailoring Written Reports for Purpose:

Format and Style:

- Formal reports: Detailed analysis with supporting evidence, tables, and charts for complex issues or high-level audiences.

- Informal reports: Summarized information and key findings for operational updates or internal communication.

- Bulletins/memorandums: Concise updates on specific issues or action items.

Key Considerations:

- Audience: Tailor language, level of detail, and tone to the specific audience (e.g., senior management, operational managers, external stakeholders).

- Purpose: Clearly define the report’s objective and what conclusions or recommendations it aims to present.

- Content:

- Executive summary: Concise overview of key findings and recommendations.

- Main body: Presents detailed analysis, evidence, and explanations.

- Conclusions and recommendations: Summarize key takeaways and actionable suggestions.

- Appendices: Include supporting data, detailed calculations, or additional information not essential for the main body.

Illustration: A cost analysis report for senior management would be a formal document with detailed cost breakdowns, charts, and recommendations for cost reduction, while a daily sales report for internal communication might be an informal email highlighting key sales figures and trends.

B. Harnessing the Power of Data Visualization:

Choosing the Right Chart:

- Bar charts: Effective for comparing categories, highlighting differences in magnitude.

- Line graphs: Track trends and changes over time, identify patterns and relationships.

- Pie charts: Represent proportions within a whole, best for limited categories.

- Scatter graphs: Reveal correlations or relationships between two variables.

Additional Considerations:

- Clarity and labeling: Ensure charts are clear, well-labeled, and easy to understand.

- Color choice: Use colors effectively to enhance clarity and avoid misleading interpretations.

- Context and explanation: Provide context and interpretation alongside the visualization to ensure proper understanding.

Illustration: A line graph showcasing monthly sales trends over a year helps identify seasonality and inform sales forecasting, while a bar chart comparing marketing campaign performance across different channels enables evaluating campaign effectiveness.

C. Decoding Information from Reports and Visualizations:

Critical Reading and Analysis:

- Identify key trends, patterns, and relationships.

- Evaluate the strength and limitations of the data and analysis.

- Consider potential biases or underlying assumptions.

- Formulate questions and seek clarification as needed.

Interpreting Visualizations:

- Understand the type of chart and its purpose.

- Read and interpret the axes, labels, and legends carefully.

- Identify major trends, outliers, and areas of interest.

- Draw conclusions and insights based on the visualization within the context of the larger report.

Illustration: Recognizing a downward trend in customer satisfaction ratings in a pie chart would prompt further investigation into the contributing factors and potential solutions mentioned in the accompanying report.