F7 – Chapter 2: Accounting for transactions in financial statements

1. Tangible Non-Current Assets

A) Definition and Initial Measurement:

- Non-current assets: Tangible assets (land, buildings, equipment) held for use beyond one year or the operating cycle.

- Initial measurement: Cost principle – acquisition cost, including borrowing costs directly attributable to acquiring the asset (capitalized during construction), incidental costs (added to cost), and less any accumulated depreciation and impairment losses.

- Self-constructed assets: Capitalize direct materials, direct labor, and other directly attributable costs incurred during construction.

b) Subsequent Expenditure:

- Capitalized: Expenditures that increase the future economic benefits of an asset or replace its parts (major repairs, upgrades).

- Expensed: Expenditures that maintain the existing economic benefits of an asset or do not enhance its future benefits (routine maintenance, repairs).

c) Revaluation:

- Requirements: IFRS 16 Property, Plant and Equipment allows revaluation to fair value, but it’s not mandatory.

- Purpose: Reflects current market value in the financial statements.

d) Revaluation Gains/Losses:

- Revaluation gain: Credited to Other Comprehensive Income (OCI).

- Revaluation loss: Recognized in profit or loss if it exceeds accumulated depreciation; otherwise, charged to OCI.

- Disposal: Revaluation gain/loss previously recognized in OCI is reclassified to profit or loss upon disposal.

e) Depreciation:

- Cost model: Allocates cost less residual value over the asset’s useful life using a systematic method (straight-line, declining balance, etc.).

- Revaluation model: Depreciates the revalued amount over the remaining useful life.

- Assets with multiple parts: Depreciate each significant part separately based on its individual useful life and residual value.

f) Investment Properties:

- Treated differently due to passive nature (held to generate rental income or capital appreciation).

- Measured at fair value through profit or loss, with changes recognized in current profit or loss.

g) Applying IFRS:

- IFRS 16 provides specific guidance on the recognition, measurement, depreciation, and impairment of property, plant, and equipment.

- Understand and apply relevant sections for each aspect of investment property accounting.

2. Intangible Non-Current Assets

a) Nature and Treatment:

- Internally generated: Developed within the entity (research costs, goodwill arising from internal development).

- Purchased: Acquired from another entity (patents, trademarks, copyrights).

- Accounting: Generally recognized at cost less accumulated amortization and impairment losses.

b) Goodwill vs. Other Intangibles:

- Goodwill:

Excess of the purchase price of a business over the fair value of its identifiable net assets.

- Other intangibles: Recognized individually based on specific identification and measurement criteria.

c) Initial Recognition and Measurement:

- Criteria: Identifiable, controlled, future economic benefits probable, measurable cost.

- Cost: Purchase price, including incidental costs directly attributable to acquiring the intangible.

d) Subsequent Accounting:

- Amortized: Recognized as an expense over the useful life using a systematic method.

- Revalued: Not generally allowed (exceptions: some biological assets, intangible assets arising from government grants).

e) Research and Development Expenditure:

Expensed: Recognized in profit or loss as incurred, unless meeting specific criteria for capitalization (internal project with technical feasibility, commercial viability, ability to measure reliable costs).

3. Impairment of Assets

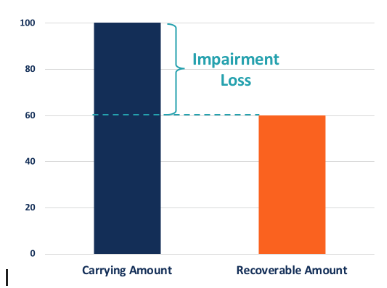

a) Impairment Loss:

- Decline in the asset’s recoverable amount (fair value less costs to sell) below its carrying amount.

- Calculation: Recoverable amount – carrying amount.

- Accounting: Recognized in profit or loss.

b) Reversal of Impairment Loss:

- Increase in the recoverable amount above the carrying amount.

- Accounting: Reversed through profit or loss, not exceeding the previously recognized impairment loss for that asset.

c) Impairment Indicators:

- Significant physical damage

- Obsolescence

- Changes in market or economic conditions

- Sudden and significant decline in the fair value of similar assets

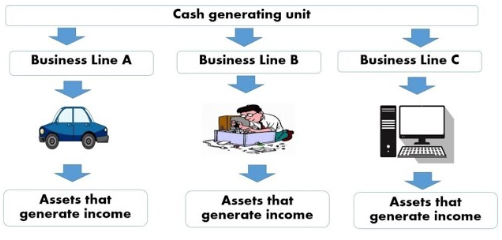

d) Cash Generating Unit (CGU):

- The smallest identifiable group of assets that generates cash inflows from its own operations or is expected to do so in the future.

- Used to allocate impairment losses.

e) Impairment Loss Allocation:

- Allocated to the assets of a CGU in proportion to their carrying amounts.

b) Applying IFRS for Biological Assets and Agricultural Produce:

- Biological assets: Living plants and animals held for sale, production of agricultural products, or breeding purposes (trees, livestock).

- Agricultural produce: Harvested product from biological assets that is ready for sale (fruits, vegetables, grains).

- Measurement: Fair value less point-of-sale costs for both biological assets and agricultural produce at the reporting date.

- Changes in fair value: Recognized in profit or loss through the income statement (biological revaluation model).

- Government subsidies: Recognized in profit or loss when the entity obtains control of the subsidy and meets the recognition criteria.

5. Financial Instruments

a) Need for a Standard:

- To ensure consistent and transparent accounting for financial instruments across different entities.

- IFRS 9 Financial Instruments addresses recognition, measurement, impairment, and hedge accounting for financial instruments.

b) Definition:

Financial assets:

Contracts that give rise to a financial asset of one entity and a financial liability or equity instrument of another entity. (Examples: receivables, loans, investments in debt or equity securities).

- Financial liabilities: Contracts that give rise to a financial liability of one entity and an asset or equity instrument of another entity. (Examples: payables, loans, bonds).

c) Factoring of Receivables:

- Sale of receivables to a third party (factor) at a discount.

- Accounting: Derecognized from the entity’s balance sheet upon sale. Gain or loss on sale recognized in profit or loss.

d) Measurement of Financial Instruments:

- Amortized cost: Applies to most financial assets held to collect contractual cash flows and financial liabilities.

- Fair value through other comprehensive income (OCI): Applies to certain financial assets not held for trading, with changes in fair value recognized in OCI and reclassified to profit or loss upon disposal.

- Fair value through profit or loss: Applies to financial assets and liabilities held for trading and certain other instruments, with changes in fair value recognized in profit or loss.

e) Debt vs. Equity:

- Debt: Fixed or determinable obligation to pay a principal amount at a maturity date, with or without interest.

- Equity: Residual interest in the assets of the entity after deducting all its liabilities.

f) Applying IFRS for Issue and Finance Costs:

- Equity: Issue costs expensed as incurred.

- Redeemable preference shares and debt instruments: Issue costs amortized over the life of the instrument and recognized as an expense in the income statement.

- Convertible debt: Issue costs allocated between the debt and equity components based on their relative fair values at issuance.

6. Leasing

a) Lessee Accounting:

- Right-of-use asset: Recognized in the balance sheet at cost, which includes the initial payment, lease payments less residual value, and any incremental borrowing costs.

- Lease liability: Recognized in the balance sheet at the present value of the remaining lease payments, discounted using the lessee’s incremental borrowing rate or the implicit rate in the lease, if known.

- Exemptions: Short-term leases (less than 12 months), low-value assets (cost below a specified threshold).

b) Sale and Leaseback:

- Transaction where an entity sells an asset and leases it back from the buyer.

- Accounting: Sale recognized at fair value, with gain or loss reflected in profit or loss. Leaseback is recognized as an operating lease unless it meets specific criteria for classification as a finance lease.

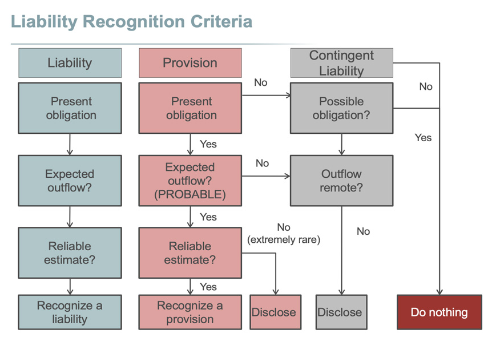

7. Provisions and Events After the Reporting Period

a) Need for a Standard:

- To ensure consistent and reliable accounting for provisions, contingent liabilities, and contingent assets.

- IFRS 37 Provisions, Contingent Liabilities and Contingent Assets addresses recognition, measurement, presentation, and disclosure of these items.

b) Legal vs. Constructive Obligations:

- Legal obligation: Arises from a past event (contractual or statutory).

- Constructive obligation: Arises from a present act (giving rise to a valid expectation in a third party that the entity will honor a particular obligation).

c) Recognition and Measurement of Provisions:

- Recognized: When an entity has a present legal or constructive obligation, a probable outflow of resources will be required to settle the obligation, and a reliable estimate of the amount can be made.

- Measured: At the present value of the amount expected to be paid to settle the obligation at the reporting date.

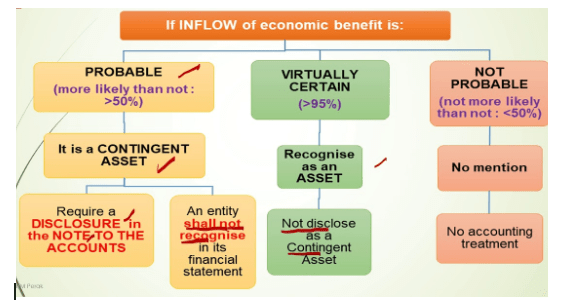

e) Contingent Assets and Liabilities:

- Contingent asset: Potential future economic benefit that arises from a past event and whose existence is uncertain or the amount cannot be reliably estimated.

- Contingent liability: Potential future obligation or expense arising from a past event whose existence is uncertain or the amount cannot be reliably estimated.

- Accounting: Disclosed in the notes to the financial statements, unless recognition criteria are met.

f) Specific Provisions:

- Warranties/guarantees: Recognize a provision when a warranty claim is probable and the cost can be reliably estimated.

- Onerous contracts: Recognize a provision for the expected loss arising from fulfilling a contract that is onerous (cost of fulfilling exceeds the economic benefits).

- Environmental, decommissioning, and similar provisions: Recognize a provision when a legal or constructive obligation exists for environmental remediation, decommissioning of assets, or similar activities.

- Restructuring: Recognize a provision for restructuring costs when a detailed restructuring plan is developed and communicated, and the entity is committed to implementing the plan.

g) Events After the Reporting Period:

- Adjusting events: Provide additional information about conditions existing at the end of the reporting period (e.g., fires, floods).

- Non-adjusting events: Occur after the reporting date but before the financial statements are authorized for issue (e.g., sale of a major subsidiary).

- Accounting: Adjusting events are reflected in the financial statements as if they had occurred at the end of the reporting period. Non-adjusting events are disclosed in the notes to the financial statements.

- Disclosures: Required for specific items after the reporting period, including their nature, financial impact, and any adjustments made to the financial statements.

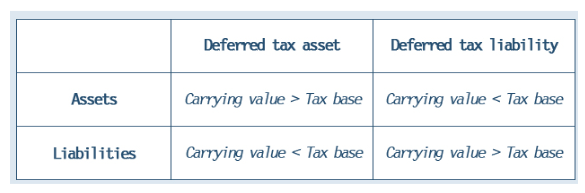

8. Taxation

a) Current Taxation:

- Recognized in profit or loss at the tax rate (tax expense), using the tax accrual basis (reflecting taxes payable and receivable).

- Deferred tax liabilities and assets are recognized to reflect the timing differences between accounting profit and taxable profit.

b) Taxable and Deductible Temporary Differences:

- Taxable temporary differences: Items included in accounting profit in one period but taxed in a future period (e.g., depreciation expense recognized in accounting records but not yet allowed for tax purposes).

- Deductible temporary differences: Items deducted in accounting profit in one period but allowed for tax purposes in a future period (e.g., research and development costs expensed in accounting records but capitalized for tax purposes).

c) Deferred Tax:

- Deferred tax liability: The present value of future tax liabilities arising from taxable temporary differences.

- Deferred tax asset: The present value of future tax benefits arising from deductible temporary differences.

- Recognition and measurement: Recognize in the financial statements unless the cumulative amount is insignificant.

9. Reporting Financial and non-financial Performance

a) Discontinued Operations:

- Separately disclosed when a component of an entity is disposed of, or its operations and cash flows are to be abandoned as a separate line of business.

b) Non-Current Assets Held for Sale and Discontinued Operations:

- Measured at the lower of carrying amount and fair value less costs to sell.

- Impairment losses:

- Recognized in other comprehensive income (OCI) if previously recognized revaluation gains are available for reclassification to profit or loss.

c) Separate Disclosure:

- Required for material items of income and expense, such as unusual items and extraordinary items.

d) Accounting Changes:

- Changes in accounting estimates: Adjusted prospectively (applying the new estimate to current and future periods), with the cumulative effect of the change recognized in current profit or loss.

- Changes in accounting policies: Adjusted retrospectively (recasting prior period financial statements as if the new policy had always been applied), with the cumulative effect recognized in current profit or loss and disclosed separately.

- Correction of prior period errors: Adjusted retrospectively by restating prior period financial statements, with the cumulative effect recognized in current retained earnings.

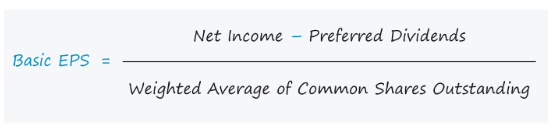

e) Earnings per Share (EPS):

- Calculation: Basic EPS = Profit after tax attributable to ordinary shareholders / Weighted average number of ordinary shares outstanding.

- Diluted EPS:

Considers the potential dilution from the exercise of convertible instruments and stock options.

f) objective, scope and core content of IFRS® Sustainability Standard 1 General Requirements for Disclosure of Sustainability-related Financial Information

Overview

In the modern financial environment, entities are expected to provide information that goes beyond traditional financial statements. Reporting financial and non-financial performance is critical for meeting stakeholders’ needs and ensuring transparency. This includes both traditional financial reporting as outlined by accounting standards and sustainability-related disclosures to address environmental, social, and governance (ESG) concerns.

Key Concepts

- Financial Performance Reporting

Financial performance reporting involves presenting information that reflects the financial health and profitability of an entity over a specified period. It includes:- Income statement (profit or loss account)

- Statement of financial position (balance sheet)

- Cash flow statement

- Notes to the financial statements

- These statements must comply with applicable International Financial Reporting Standards (IFRS), such as IFRS 15 (Revenue from Contracts with Customers) and IFRS 16 (Leases).

- Non-Financial Performance Reporting

Non-financial performance reporting focuses on disclosing information that affects an entity’s ability to create value over the short, medium, and long term. It includes:- Environmental metrics (e.g., carbon footprint, energy consumption)

- Social metrics (e.g., employee diversity, community engagement)

- Governance metrics (e.g., board composition, anti-corruption practices)

- Non-financial performance reporting aligns with frameworks such as the Global Reporting Initiative (GRI), Sustainability Accounting Standards Board (SASB), and more recently, the IFRS Sustainability Standards.

IFRS Sustainability Standard 1: General Requirements for Disclosure of Sustainability-related Financial Information

Objective

The primary objective of IFRS Sustainability Standard 1 (IFRS S1) is to establish a global baseline for sustainability-related financial disclosures. It ensures entities provide comprehensive, relevant, and comparable information about sustainability-related risks and opportunities that could affect an entity’s cash flows, financial position, or performance.

Scope

The scope of IFRS S1 applies to all entities that prepare general-purpose financial reports under IFRS. It requires disclosure of information about:

- Sustainability-related risks and opportunities: Entities must identify and disclose risks and opportunities that could significantly impact their business model or financial performance.

- Governance processes: An explanation of how governance structures oversee sustainability-related matters.

- Strategy and decision-making: How sustainability-related risks and opportunities are integrated into the entity’s strategic planning and business activities.

- Risk management: Processes to identify, assess, and manage sustainability-related risks.

- Metrics and targets: Quantitative and qualitative measures used to evaluate progress toward managing sustainability-related risks and achieving sustainability-related goals.

Core Content of IFRS S1

- Materiality:

Entities are required to disclose sustainability-related financial information that is material to users of general-purpose financial reporting. Information is considered material if its omission or misstatement could influence the decisions of investors, lenders, and other creditors. - Connectivity of Information:

Sustainability-related disclosures must be interconnected with financial statements to provide a cohesive narrative about the entity’s overall performance and risk profile. - Disclosures on Governance:

- The governance structure overseeing sustainability-related matters.

- Roles and responsibilities of the board and management in addressing sustainability-related issues.

- Strategy Disclosures:

- Description of sustainability-related risks and opportunities.

- Potential impacts on business models, strategy, and financial performance.

- Adjustments made to address identified risks and opportunities.

- Risk Management Disclosures:

- Identification and assessment of sustainability-related risks.

- Processes used to prioritize and manage these risks.

- Integration of risk management into the broader enterprise risk framework.

- Metrics and Targets:

- Disclosure of specific, measurable metrics and targets for monitoring sustainability-related performance.

- Examples include carbon emissions (Scope 1, 2, and 3), energy efficiency metrics, and progress toward net-zero goals.

Illustrations and Theoretical Applications

Illustration 1: Governance Disclosures

Company A discloses its governance framework for sustainability, highlighting that the board of directors reviews climate-related risks quarterly. The company has established a sustainability committee responsible for monitoring progress toward net-zero emissions and ensuring compliance with regulatory requirements.

Illustration 2: Strategy Disclosures

Company B, a manufacturer, identifies a significant opportunity in transitioning to renewable energy sources. Its disclosure outlines:

- A strategic decision to invest $50 million in solar energy infrastructure over five years.

- Expected cost savings of $10 million annually from reduced energy costs.

- An anticipated 40% reduction in greenhouse gas emissions.

Illustration 3: Metrics and Targets

Company C, a logistics firm, reports the following sustainability-related metrics:

- Scope 1 emissions: 500,000 metric tons CO2e.

- Scope 2 emissions: 100,000 metric tons CO2e.

- Target: 30% reduction in combined Scope 1 and 2 emissions by 2030.

Importance of Reporting Financial and Non-Financial Performance

- Enhanced Stakeholder Confidence:

Transparent reporting fosters trust among investors, customers, and regulators, enhancing the entity’s reputation. - Value Creation:

By addressing sustainability-related risks and opportunities, entities can identify cost-saving measures, drive innovation, and ensure long-term profitability. - Regulatory Compliance:

As sustainability reporting becomes mandatory in many jurisdictions, entities complying with IFRS S1 are well-positioned to meet global requirements. - Improved Risk Management:

Integration of financial and non-financial reporting helps entities better understand and mitigate risks associated with sustainability-related challenges.

By combining financial and non-financial reporting, entities can provide a comprehensive view of their overall performance and resilience in a rapidly evolving business landscape.

10. Revenue

a) Principles of Revenue Recognition:

- Identification of contracts: Identify the performance obligations (goods or services) promised to the customer in the contract.

- Identification of performance obligations: Identify the distinct performance obligations within the contract that can be separately identified and delivered to the customer.

b) Principles of Revenue Recognition (continued):

- Allocation of the price to performance obligations: Allocate the transaction price to the identified performance obligations based on their relative standalone selling prices (or fair value if more readily determinable).

- Recognition of revenue when/as performance obligations are satisfied: Recognize revenue when (or as) the entity transfers control of a promised good or service to the customer.

c) Revenue Recognition over Time vs. At a Point in Time:

- Over time: Recognized as the entity satisfies its performance obligations (e.g., construction contracts, long-term service contracts).

- At a point in time: Recognized upon transfer of control of the promised good or service (e.g., sale of goods, rendering of services).

d) Progress Towards Complete Satisfaction:

- Percentage-of-completion method: Revenue recognized based on the estimated percentage of performance obligations completed at the reporting date.

- Input method: Revenue recognized based on the resources used to complete the performance obligations relative to the total expected resources to be used.

e) Recognition of Contract Costs:

- Recognized as an expense in the period they are incurred, unless they meet specific criteria for capitalization (directly attributable to the identified performance obligations).

f) Specific Revenue Recognition Examples:

- Principal vs. Agent: Principal recognizes revenue upon sale; Agent recognizes a commission when the sale is made.

- Repurchase Agreements: Sale is not recognized; treated as a secured financing arrangement.

- Bill and Hold Arrangements: Customer has not taken legal title; sale is not recognized.

- Consignment Arrangements: Consignor recognizes revenue when the consignee sells the goods.

g) Financial Statement Extracts:

- Prepare separate financial statement extracts for contracts where performance obligations are satisfied over time or at a point in time, including:

- Description of the contract

- Performance obligations

- Transaction price allocation

- Progress towards completion (if applicable)

- Recognized revenue and contract costs

11. Government Grants

a) Applying IFRS:

- IFRS 12 Grants defines the recognition, measurement, and presentation of government grants.

- Grants are recognized as income when the entity obtains control over the grant and meets the specific conditions for recognition.

- Grants may be measured at fair value or at the present value of the expected cash inflows from the grant.

- Grants related to the cost of an asset are recognized as deferred income and credited to profit or loss as the asset is depreciated.

12. Foreign Currency Transactions

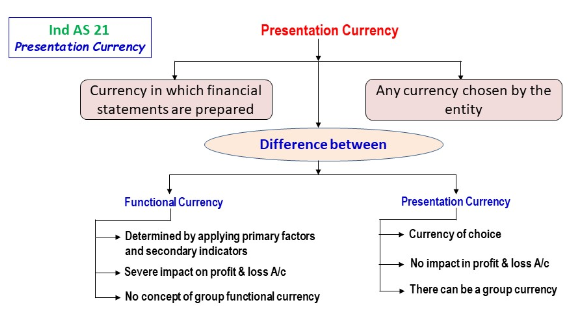

a) Functional and Presentation Currency:

- Functional currency: The primary currency in which the entity generates and expends cash (generally the currency of the economic environment in which the entity operates).

- Presentation currency: The currency in which the financial statements are presented.

- Adjustments: Foreign currency transactions and monetary/non-monetary foreign currency items are translated to the presentation currency using appropriate exchange rates.

b) Accounting for Foreign Currency Transactions:

- Translation of foreign currency transactions: Recognized in profit or loss at the exchange rate prevailing on the transaction date.

- Translation of monetary/non-monetary foreign currency items: Recognized in other comprehensive income (OCI) at the exchange rate prevailing at the reporting date, with accumulated amounts reclassified to profit or loss upon settlement.