SBR INT – Chapter 1: Fundamental ethical and professional principles

Topic 1: Professional and Ethical Behavior in Corporate Reporting

a) Importance of Ethical and Professional Behaviour in Complying with Accounting Standards and Corporate Reporting Requirements

Theories:

- Ethical Theory: This broad umbrella encompasses various philosophical perspectives on right and wrong conduct. Relevant theories within this context include:

- Deontology: Focuses on the inherent moral rightness or wrongness of actions, regardless of the consequences. In accounting, this translates to upholding principles like honesty, integrity, and objectivity, irrespective of pressure or incentives.

- Utilitarianism:

Promotes actions that maximize overall happiness or well-being. In corporate reporting, this means preparing reliable and accurate financial statements that serve the best interests of all stakeholders, not just management’s self-interest.

- Virtue Ethics: Emphasizes developing and embodying virtues like honesty, fairness, and prudence in one’s professional conduct. Upholding these virtues translates to ethical decision-making in the face of challenging situations.

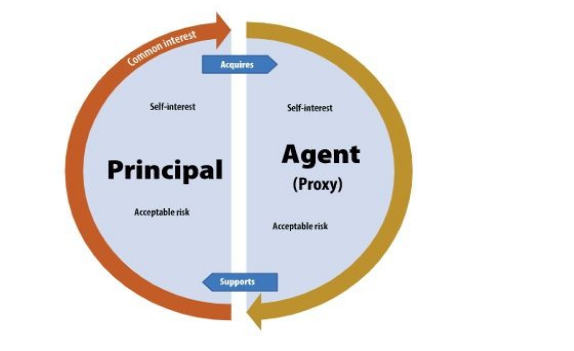

- Agency Theory:

This theory posits that managers act as agents for the owners (principals) of a company. The agency problem arises when managers’ interests diverge from those of the owners, potentially leading to self-serving actions. Ethical and professional behaviour helps mitigate this agency problem by ensuring managers act in the best interests of the owners and stakeholders.

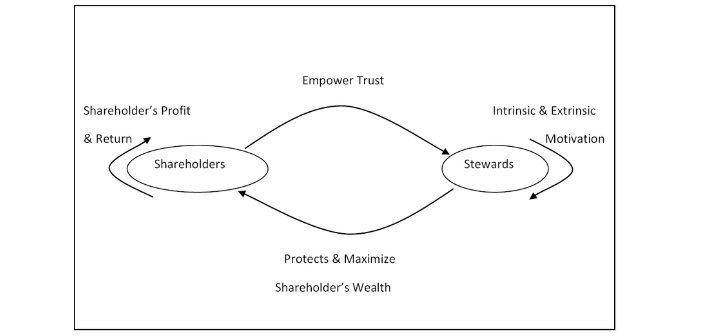

- Stewardship Theory:

This theory views managers as stewards entrusted with the resources and responsibility of the company for the benefit of all stakeholders. This perspective emphasizes ethical leadership and responsible financial reporting to ensure the long-term sustainability and success of the company.

Illustrations:

- Maintaining public trust in financial markets: Ethical and professional behavior in corporate reporting is crucial for maintaining public trust in the financial markets. Accurate and reliable financial statements enable investors and other stakeholders to make informed decisions based on true financial information.

- Enhancing corporate reputation: Upholding ethical standards strengthens an organization’s reputation. Investors and other stakeholders are more likely to invest in and do business with companies with a strong ethical track record and commitment to transparent reporting.

- Reducing the risk of fraud and misconduct: Following ethical principles helps minimize the risk of fraudulent activities and financial reporting manipulations. This protects the company from financial and reputational damage, safeguarding its long-term viability.

- Attracting and retaining talent: A company known for its ethical conduct attracts and retains high-quality employees who share similar values. This fosters a positive work environment and promotes overall organizational success.

ACCA IFRS Sustainability Disclosure Standards S1: A Comprehensive Overview

Introduction

The International Financial Reporting Standards (IFRS) Sustainability Disclosure Standard S1 is a key framework developed to improve the consistency and transparency of sustainability-related financial disclosures. Introduced by the International Sustainability Standards Board (ISSB), S1 aims to standardize the way companies report their sustainability-related risks and opportunities, ensuring that investors and stakeholders have access to high-quality, comparable information.

As the Association of Chartered Certified Accountants (ACCA) supports the adoption of these standards, this document provides a detailed exploration of IFRS S1, its scope, requirements, and implications for businesses worldwide.

Background and Objectives

The need for sustainability disclosure standards has grown significantly due to increasing global concerns over climate change, corporate governance, and social responsibility. Investors and regulators demand greater transparency in how businesses manage environmental, social, and governance (ESG) risks.

The ISSB developed IFRS S1 alongside IFRS S2, which specifically addresses climate-related disclosures. S1 focuses on general sustainability-related financial disclosures, establishing a comprehensive framework that companies can use to communicate sustainability-related information effectively.

Objectives of IFRS S1

- Enhance Transparency: Provide investors with clear, comparable, and reliable sustainability-related information.

- Improve Decision-Making: Support informed decision-making by disclosing sustainability risks and opportunities.

- Ensure Global Consistency: Align sustainability reporting practices across industries and jurisdictions.

- Integrate with Financial Reporting: Complement existing financial reporting frameworks, such as IFRS and Generally Accepted Accounting Principles (GAAP).

Scope and Applicability

Who Must Comply?

IFRS S1 applies to all entities that are required or choose to prepare sustainability-related financial disclosures. It is particularly relevant to:

- Publicly listed companies

- Financial institutions

- Large corporations with significant sustainability risks

- Entities seeking investment from ESG-conscious stakeholders

While initially designed for large corporations, regulators may extend its application to small and medium-sized enterprises (SMEs) in the future.

Key Disclosure Areas

IFRS S1 requires companies to disclose material information about sustainability-related risks and opportunities that could reasonably be expected to affect their cash flows, access to finance, or cost of capital. The disclosures should cover:

- Governance

- How sustainability responsibilities are assigned within the organization

- The role of the board and management in overseeing sustainability risks

- Strategy

- The entity’s approach to managing sustainability-related risks and opportunities

- The impact of sustainability factors on business models and strategy

- Risk Management

- Processes used to identify, assess, and manage sustainability risks

- Integration of sustainability risk management within enterprise risk management frameworks

- Metrics and Targets

- Key sustainability performance indicators (KPIs)

- Quantitative and qualitative targets related to sustainability objectives

Implementation and Compliance Challenges

Challenges Companies May Face

While IFRS S1 aims to streamline sustainability reporting, businesses may face several challenges in implementing the standard:

- Data Collection: Companies may struggle with gathering reliable and standardized sustainability data.

- Resource Allocation: Significant investments may be required in technology, personnel, and training.

- Alignment with Existing Frameworks: Companies using other sustainability standards, such as Global Reporting Initiative (GRI) or Task Force on Climate-related Financial Disclosures (TCFD), may need to align their reporting processes.

- Regulatory Variations: Different jurisdictions may adopt IFRS S1 at different rates, leading to inconsistent compliance expectations.

Steps for Effective Implementation

To ensure a smooth transition to IFRS S1 compliance, businesses can follow these steps:

- Assess Readiness: Evaluate current sustainability reporting practices and identify gaps.

- Engage Stakeholders: Educate internal teams, investors, and regulatory bodies about IFRS S1 requirements.

- Develop a Reporting Framework: Establish internal guidelines for collecting, analyzing, and reporting sustainability data.

- Invest in Technology: Use digital tools and software to streamline data management and reporting.

- Ensure Continuous Monitoring: Regularly update and refine sustainability reporting processes based on evolving standards and regulations.

The Role of ACCA in IFRS S1 Adoption

The Association of Chartered Certified Accountants (ACCA) plays a crucial role in supporting IFRS S1 adoption by:

- Providing Guidance and Training: ACCA offers training programs and materials to help finance professionals understand and implement IFRS S1.

- Advocating for Global Adoption: ACCA collaborates with regulatory bodies to promote the standard’s adoption worldwide.

- Encouraging Best Practices: The organization publishes research, case studies, and practical insights on sustainability reporting.

b) Consequences of Unethical Behavior by Management in Corporate Reporting

Theories:

- Agency Theory: When management engages in unethical behaviour in corporate reporting, it exacerbates the agency problem. This can lead to:

- Information asymmetry: Management withholds or misrepresents crucial financial information, hindering informed decision-making by stakeholders.

- Wealth transfer: Shareholders suffer losses, while management may benefit through self-serving actions, such as manipulating financial statements to boost stock prices.

- Market inefficiencies: Unethical practices distort the market by creating an unlevel playing field and hindering efficient allocation of resources.

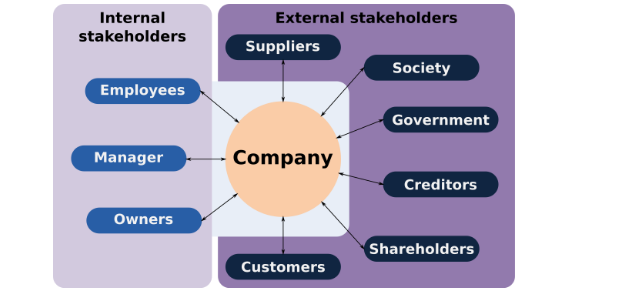

- Stakeholder Theory:

Unethical behaviour by management harms various stakeholders, including:

- Investors: Suffer financial losses due to inaccurate or misleading financial information.

- Employees: May lose jobs or face uncertainty due to potential company collapse or reputational damage.

- Creditors: Increased risk of loan defaults due to financial instability caused by unethical reporting.

- Public: May lose trust in the financial system and suffer negative economic consequences from market inefficiencies.

Illustrations:

- The Enron Scandal: This infamous example showcased how unethical accounting practices led to the company’s collapse, causing billions of dollars in losses for investors and employees.

- The Volkswagen Emissions Scandal: The company’s manipulation of emissions data resulted in significant financial penalties, reputational damage, and a loss of consumer trust.

- Corporate fines and penalties: Regulatory bodies impose hefty fines on companies engaging in unethical reporting practices.

- Legal repercussions: Management may face criminal charges and personal liability for their actions.

Conclusion

Ethical and professional behavior in corporate reporting is paramount for maintaining public trust, protecting stakeholders’ interests, and ensuring the long-term sustainability of companies. Conversely, unethical conduct by management can have devastating consequences, leading to financial losses, reputational damage, and legal repercussions. By understanding the importance of ethical behavior and the potential consequences of its absence, professionals involved in corporate reporting can contribute to a more transparent and responsible financial system.