What is and how to achieve financial freedom and steps to achieve

What is and how to achieve financial freedom and steps to achieve

What is Financial Freedom?

Definition:

Financial freedom is the state where an individual has enough financial resources—such as investments, savings, or passive income—to sustain their lifestyle indefinitely, without being dependent on a regular job or active income. It’s about achieving a level of financial independence where your income covers expenses, allowing you to pursue other interests, hobbies, and life goals.

At its core, financial freedom provides a sense of security, autonomy, and the ability to make choices based on personal desires rather than financial necessity.

Benefits

Financial freedom offers numerous benefits beyond simply having more money. Here’s a deeper look into these advantages:

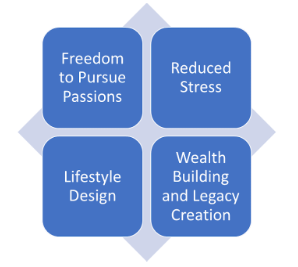

- Freedom to Pursue Passions: With financial independence, individuals can dedicate time to hobbies, personal growth, travel, and causes that matter to them. This flexibility allows people to engage in activities they enjoy without worrying about monetary constraints.

- Reduced Stress: Financial stress often stems from the fear of not being able to meet basic needs. With financial freedom, individuals experience reduced anxiety, knowing that their basic expenses are covered and that they have the flexibility to handle unexpected costs without debt.

- Lifestyle Design: Financial freedom empowers people to design their lives according to their values and priorities. Whether that means retiring early, working part-time, or dedicating time to philanthropic efforts, it opens up opportunities for intentional living.

- Wealth Building and Legacy Creation: Beyond personal enjoyment, financial independence allows individuals to create and pass down generational wealth. Establishing trusts, wills, and estate planning ensures that the fruits of one’s labor continue to support future generations or charitable causes.

Steps to Achieve Financial Freedom

To achieve financial freedom, a well-structured plan that incorporates various steps is crucial. These steps guide individuals through a disciplined approach to managing finances, building wealth, and securing a future free from financial constraints. Below is a detailed breakdown of each step needed to achieve financial freedom.

1. Budgeting and Saving

a) Creating a Budget

Creating a budget is the foundation of financial success. A budget provides a clear view of your financial situation, allowing you to allocate your income towards expenses, savings, and investments effectively.

i. Tracking Income and Expenses:

- Start by recording all sources of income, including wages, bonuses, freelance work, rental income, or any other revenue streams.

- Track every expense, categorizing them into essential expenses (e.g., rent, utilities), discretionary spending (e.g., dining out, entertainment), and savings contributions.

ii. Benefits of Budgeting:

- Helps control spending habits.

- Identifies areas where you can save more.

- Offers a roadmap to reach financial goals.

iii. Creating a Simple Budget:

- Income: List all income sources and calculate the total monthly income.

- Expenses: Break down expenses into fixed, variable, and discretionary spending.

- Savings and Investments: Allocate funds toward savings goals (emergency fund, retirement, investment accounts) after covering expenses.

Zero-Based Budgeting: A popular method where every dollar earned is allocated to a specific expense, saving, or investment category, ensuring that no funds are left unused.

b) Reducing Expenses

Reducing expenses is a critical component of achieving financial freedom. By trimming unnecessary costs, you create more room for savings and investments.

i. Identifying Unnecessary Spending:

- Track discretionary spending—impulse purchases, luxury goods, dining out, and entertainment expenses—that may be cut back or eliminated.

- Cancel unused subscriptions, memberships, or services that do not align with financial goals.

ii. Cutting Back Without Sacrificing Quality of Life:

- Focus on value-based spending where you prioritize spending on things that matter most.

- Example: Opting for home-cooked meals instead of dining out frequently or driving instead of flying to reduce travel expenses.

iii. Automating Savings: Set up automatic transfers to savings accounts or investment vehicles to ensure consistent saving behavior without requiring constant monitoring.

c) Building an Emergency Fund

An emergency fund is essential for financial stability. It serves as a financial safety net for unexpected expenses like medical bills, car repairs, or job loss.

i. Why an Emergency Fund is Important:

- Helps prevent reliance on high-interest debt during financial emergencies.

- Reduces stress during unforeseen situations by providing a buffer against financial surprises.

ii. Steps to Build an Emergency Fund:

- Determine Fund Size: Aim to save 3 to 6 months’ worth of living expenses.

- Set a Monthly Goal: Start small and gradually increase savings to reach the target.

- Choose the Right Account: Place emergency funds in a high-yield savings account or money market account to earn some interest while keeping funds accessible.

Utilizing Windfalls: Consider contributing extra income, tax refunds, or bonuses to the emergency fund for faster accumulation.

2. Increasing Income

Increasing income is a vital step towards financial freedom. By boosting earnings, you create opportunities to invest, save, and build wealth more effectively.

i. Career Growth

Career growth involves continuously developing your skills to secure higher-paying roles and better job opportunities. This can be achieved through education, training, and networking.

ii. Upskilling:

- Gain specialized certifications or knowledge in your field that make you more marketable.

- Take advantage of online learning platforms (e.g., Coursera, Udemy) to acquire relevant skills.

iii. Advancing Your Career:

- Seek promotions by demonstrating your value through achievements and contributions.

- Stay proactive in building relationships within your industry to unlock new opportunities.

iv. Negotiating Salary Increases:

- Research industry standards for your role and prepare to present your achievements and contributions during performance reviews or salary negotiations.

a) Side Hustles

A side hustle can provide additional income streams that can be funneled into savings, investments, or future ventures. Many people use side hustles as a means to generate supplemental income without leaving their primary job.

Popular Side Hustles:

- Freelancing (writing, graphic design, web development).

- Gig economy jobs (ride-sharing, food delivery).

- E-commerce (selling products through platforms like Etsy, Amazon).

- Consulting or coaching in your area of expertise.

Scaling Side Hustles: Focus on creating systems to automate certain aspects, such as marketing or inventory management, to increase efficiency and profits.

b) Passive Income Streams

Passive income provides ongoing earnings with minimal effort. These streams are integral to building wealth for the long term.

i. Investments in Real Estate:

- Rental properties or real estate investment trusts (REITs) offer a reliable source of income while allowing for potential appreciation in property values.

- Consider property management companies to handle day-to-day operations, reducing time spent actively managing properties.

ii. Investments in Stocks:

- Dividend stocks generate regular payouts while allowing long-term capital appreciation.

- Index funds and exchange-traded funds (ETFs) provide diversified, low-cost options to build passive income over time.

iii. Creating Digital Products:

- Build and sell digital assets like courses, eBooks, or software applications, which can generate income passively after initial setup.

3. Eliminating Debt

Eliminating debt is a critical step in achieving financial freedom. Debt can consume a significant portion of your income, leaving little room for savings and investments. Developing an effective strategy to manage and reduce debt allows you to redirect funds toward building wealth and achieving financial independence.

a) Creating a Debt Repayment Plan

A well-structured debt repayment plan is essential for systematically addressing and reducing outstanding debt. This approach helps avoid accumulating more debt while ensuring you make consistent progress toward financial freedom.

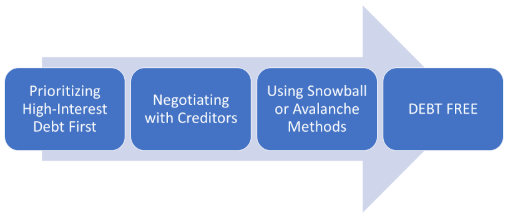

i. Prioritizing High-Interest Debt First:

- High-interest debt, such as credit card debt, tends to accumulate rapidly due to compounded interest. Prioritizing these debts minimizes the overall cost of repayment.

- Use methods like the Avalanche Method, which targets debts with the highest interest rates first, to reduce interest payments and free up funds faster.

ii. Steps to Create a Debt Repayment Plan:

- Assess All Debts: Compile a list of all debts, including credit card balances, personal loans, student loans, mortgages, and any other obligations.

- Determine Minimum Payments: Make the minimum payment on all debts while focusing excess funds on high-interest debts.

- Focus on One Debt at a Time: Apply extra funds toward the smallest or highest-interest debt, depending on the method used.

- Track Progress: Monitor reductions in debt and adjust the repayment plan as needed.

b) Negotiating with Creditors

Negotiating with creditors is an effective way to reduce the financial burden of debt, particularly for those struggling to meet minimum payments or those facing financial hardship.

i. Options for Negotiation:

- Reduced Interest Rates: Request a lower interest rate, which can significantly lower monthly payments and the total repayment amount.

- Debt Settlement: Offer a lump sum payment that is less than the total owed to settle the debt, which is often accepted by creditors to avoid lengthy legal proceedings.

ii. Steps for Negotiating:

- Prepare Documentation: Gather all necessary information about your financial situation, including debts owed, income, and monthly expenses.

- Reach Out to Creditors: Contact creditors directly or use professional debt relief services.

- Document Agreements: Ensure all negotiated terms are documented in writing to avoid misunderstandings.

c) Using Snowball or Avalanche Methods

The Snowball and Avalanche methods are popular strategies for repaying debt efficiently, offering different psychological and financial benefits.

Snowball Method: Focuses on paying off the smallest debts first to build momentum and a sense of accomplishment. This is ideal for those who need motivation to keep moving forward.

- Steps: Start by paying the minimum on all debts except the smallest one, to which you allocate the highest possible payments. Once the smallest debt is paid off, move on to the next smallest debt.

Avalanche Method: Prioritizes paying off high-interest debts first to minimize the total cost of repayment. This method saves the most money over time.

- Steps: Apply all extra funds toward the highest-interest debt until it’s fully paid off, then move to the next highest-interest debt.

Both methods aim to eliminate debt systematically, but the Avalanche method often results in faster financial freedom as it reduces interest payments substantially.

4. Investing for Wealth Building

Investing is a powerful tool for wealth-building and a critical component of achieving financial freedom. A well-balanced investment strategy minimizes risk while leveraging compound growth to accelerate wealth accumulation.

a) Types of Investments

Investing involves allocating resources toward assets with the expectation of generating income or capital appreciation. Below are some of the most common investment vehicles:

i. Stocks: Represent ownership in a company. Stocks offer the potential for high returns but come with higher risk due to market volatility.

- Growth Stocks: Companies expected to grow rapidly.

- Dividend Stocks: Provide regular dividend payments in addition to potential price appreciation.

ii. Bonds: Fixed-income securities issued by governments or corporations to raise capital. Bonds offer lower returns compared to stocks but with lower risk.

b) Types of Bonds:

- Government Bonds: Considered low-risk, offering steady returns.

- Corporate Bonds: Issued by companies and typically provide higher returns but at higher risk.

iii. Real Estate: Investment in property or real estate can provide rental income and capital appreciation over time.

- REITs (Real Estate Investment Trusts) allow individuals to invest in real estate without managing properties directly.

iv. Index Funds and ETFs: Low-cost, diversified investment options that track the performance of a specific index (e.g., S&P 500), providing exposure to a wide range of assets and sectors with minimal effort.

c) Risk Management

Effective risk management is essential for long-term investment success. Diversifying investments across different asset classes minimizes risk exposure and protects against market volatility.

i. Types of Diversification:

- Geographic Diversification: Investing in assets across different countries or regions.

- Asset Class Diversification: Balancing stocks, bonds, real estate, and alternative investments (e.g., commodities, cryptocurrencies).

- Industry Diversification: Spreading investments across various industries (e.g., technology, healthcare, finance) to reduce dependency on a single sector.

ii. Rebalancing Portfolios: Regularly adjusting your portfolio to maintain the desired level of diversification, balancing risk and return according to investment goals.

d) Compounding

Compounding is a key driver of wealth accumulation over time. It allows returns on investments to generate even greater returns through reinvestment of profits.

i. Power of Compounding:

- Interest Compounded: Regular reinvestment of interest or dividends earned on an investment.

- Capital Gains Reinvestment: Using profits from asset sales to purchase more investments.

ii. Benefits:

- Accelerates wealth growth exponentially over time.

- Helps in minimizing the impact of market fluctuations through consistent reinvestment.

iii. Long-Term Focus: The earlier you start investing and the longer you let your investments compound, the greater the potential for wealth accumulation.

5. Financial Planning and Goal Setting

Effective financial planning and goal setting are essential components of achieving financial freedom. By setting clear, actionable financial goals and creating a roadmap for achieving them, individuals can better align their financial decisions with their long-term aspirations. This process involves setting SMART goals, planning for retirement, and ensuring proper estate planning.

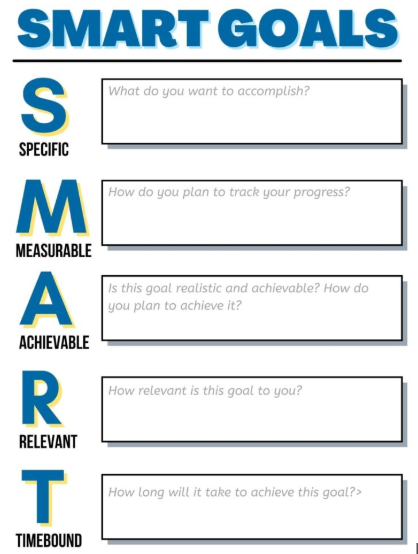

a) Setting SMART Goals

SMART goals provide a structured framework for setting financial objectives. By ensuring that goals are specific, measurable, achievable, relevant, and time-bound, individuals can track their progress and remain motivated.

- Specific: Clearly define what you want to achieve. For example, instead of saying “save more money,” specify “save $10,000 for a down payment on a home within the next 3 years.”

- Measurable: Establish a way to track progress. This could be through numbers, percentages, or milestones. For instance, tracking how much you save each month toward your financial goal.

- Achievable: Ensure that goals are realistic given your current financial situation and resources. A goal should push you to stretch, but not be so ambitious that it becomes unattainable.

- Relevant: Align goals with your overall financial priorities and values. For example, setting a goal to travel the world may not be relevant if retirement planning is your top priority.

- Time-bound: Establish a deadline for achieving the goal, which creates a sense of urgency and allows for consistent effort toward completion.

- Example of SMART Goal: Save $2,000 in a year by contributing $167 per month toward an emergency fund.

b) Retirement Planning

Retirement planning is critical for ensuring financial security in the later stages of life. It involves assessing your current financial situation, projecting future expenses, and investing to accumulate enough wealth to support your lifestyle during retirement.

i. Types of Retirement Accounts:

- 401(k): Employer-sponsored retirement savings plan with employer matching contributions.

- IRA: Individual Retirement Account, offering tax advantages such as Traditional IRA (deductible contributions) or Roth IRA (tax-free withdrawals).

- Pensions: Retirement plans where employers guarantee a certain level of income after retirement, typically based on years of service and salary history.

ii. Steps for Retirement Planning:

- Assess Current Savings: Evaluate how much has been saved toward retirement.

- Estimate Future Expenses: Consider healthcare costs, lifestyle needs, and inflation when projecting future expenses.

- Choose Investment Strategies: Diversify retirement accounts with stocks, bonds, mutual funds, or real estate for a balanced approach.

- Review Regularly: Continuously assess progress toward retirement goals and adjust as needed.

c) Estate Planning

Estate planning ensures that wealth is distributed according to your wishes after you pass away. It involves creating legal documents to protect assets and minimize taxes.

i. Key Components:

- Wills: Legal documents outlining how you want your assets distributed.

- Trusts: Used to manage assets, minimize taxes, and ensure wealth is passed on to beneficiaries in a controlled manner.

- Power of Attorney: Appointing someone to make financial decisions on your behalf if you become incapacitated.

- Healthcare Directives: Documents specifying medical treatment preferences if you are unable to make decisions.

ii. Importance of Estate Planning:

- Avoids probate, which can be costly and time-consuming.

- Provides clarity on who will inherit assets, reducing disputes among family members.

- Helps protect minor children by naming guardians and setting up trusts for their financial needs.

6. Continuous Education and Tracking

Achieving and maintaining financial freedom requires ongoing education and regular tracking of financial progress. Staying informed about financial literacy and regularly adjusting financial plans ensures that you stay on the right path toward your goals.

a) Financial Literacy

Financial literacy is the foundation of smart financial decision-making. It involves understanding essential personal finance concepts, such as budgeting, saving, investing, and debt management.

i. Benefits of Financial Literacy:

- Increases awareness of financial products and services.

- Builds confidence in managing personal finances.

- Provides the knowledge to make informed financial decisions that lead to wealth accumulation.

ii. Ways to Enhance Financial Literacy:

- Reading Financial Books: Books like “The Intelligent Investor” by Benjamin Graham or “Rich Dad Poor Dad” by Robert Kiyosaki.

- Online Resources: Utilize personal finance websites, blogs, and educational platforms (e.g., Khan Academy, Finopedia) for tutorials and articles.

- Financial Workshops and Seminars: Attend events to gain practical insights from industry professionals.

b) Review and Adjust

Continuous tracking and adjusting your financial plans ensure that you are aligned with changing personal circumstances, economic conditions, and financial goals.

i. Why Regular Reviews Are Essential:

- Life events such as marriage, childbirth, or career changes can necessitate adjustments in financial goals.

- Economic fluctuations, market conditions, and inflation can impact investment returns and savings plans.

ii. Steps for Reviewing and Adjusting:

- Monitor Key Financial Metrics: Regularly check savings balances, investment performance, and debt levels.

- Evaluate Progress: Compare progress toward goals with your initial plan.

- Adjust Strategies: Reassess and tweak budget allocations, investment strategies, and debt repayment plans as necessary.

Tools for Tracking: Use budgeting apps like Mint, Personal Capital, or spreadsheets to keep track of financial data systematically.

You are now Financially Free!

By combining robust financial planning with continuous education and regular adjustments, individuals can create a sustainable path toward achieving financial freedom. Whether through setting SMART goals, planning for retirement, or ensuring proper estate management, each step is integral to building a secure, prosperous financial future.

Real-Life Illustration: Achieving Financial Freedom

Scenario: Meet Sarah, the Nurse

Sarah is a licensed practical nurse (LPN) who dreams of achieving financial freedom—the ability to make life decisions without being overly stressed about money because she has sufficient savings, investments, and income streams. Let’s follow Sarah’s journey to financial freedom step by step.

What is Financial Freedom in Sarah’s Perspective?

Financial freedom means being in control of your finances and living comfortably without depending on each paycheck. For Sarah, it means:

- Paying off her student loans.

- Saving for a home.

- Investing for retirement.

- Having enough financial security to travel and care for her family without stressing over unexpected expenses.

Steps to Achieve Financial Freedom

1. Set Clear Financial Goals

Sarah starts by defining her financial freedom goals:

- Save $30,000 for a down payment on a house within five years.

- Pay off her $20,000 student loan in three years.

- Build an emergency fund equal to three months of expenses.

- Invest for retirement to ensure she can retire by 60.

She writes down her goals, making them specific, measurable, and time-bound.

2. Create a Budget

Sarah tracks her monthly income ($4,000 after taxes) and expenses. She identifies areas where she can save, such as eating out less and shopping more mindfully. Her new budget includes:

- Rent: $1,200

- Groceries: $400

- Transportation: $200

- Student Loan Payment: $600 (increased to pay off faster)

- Savings: $800

By sticking to this budget, Sarah ensures she lives below her means.

3. Pay Off Debt

Sarah uses the debt snowball method(To add definition within content):

- She lists all her debts (student loans, a $5,000 car loan, and a $2,000 credit card balance) from smallest to largest.

- She aggressively pays off the credit card first while making minimum payments on the others.

- Once the credit card is paid off, she focuses on the car loan and finally the student loans.

This approach keeps her motivated as she sees quick wins.

4. Build an Emergency Fund

Sarah saves three months’ worth of living expenses ($9,000) in a high-yield savings account. This gives her peace of mind to handle unexpected expenses, like medical bills or car repairs.

5. Invest for the Future

Sarah starts investing in her employer’s 401(k) plan, contributing 10% of her income. Her employer matches 4%, giving her free money for retirement. She also opens a Roth IRA and sets up automatic monthly contributions of $200.

6. Diversify Income Streams

To accelerate her financial goals, Sarah starts a side hustle: tutoring nursing students for the NCLEX-PN exam. She earns an additional $500 monthly, which she uses to boost her savings and investments.

7. Educate Herself About Money

Sarah reads books on personal finance, listens to podcasts, and attends workshops to improve her financial literacy. She learns about investing, taxes, and how to build wealth over time.

8. Stay Disciplined and Adjust as Needed

Life throws unexpected challenges at Sarah, like a car repair and a medical expense. However, her emergency fund covers these costs, and she stays disciplined, continuing to follow her financial plan.

Outcome: Financial Freedom

After six years, Sarah achieves her version of financial freedom:

- She’s debt-free.

- She owns her home with a 20% down payment saved.

- She has $25,000 invested in retirement accounts and continues to grow her wealth.

- She has a fully funded emergency fund.

Now, Sarah can work fewer hours, take vacations, and even support her family without financial stress. She enjoys the freedom to make choices based on what she values, not just her income.

Key Takeaways for Financial Freedom

- Define clear goals.

- Create and stick to a budget.

- Pay off debt systematically.

- Save for emergencies.

- Invest early and consistently.

- Diversify income streams.

- Educate yourself about personal finance.

- Stay disciplined and adapt as needed.

Sarah’s journey is a realistic and practical example of how anyone can achieve financial freedom with determination, planning, and smart financial habits.

The Value of a Financial Advisor

While this article offers valuable insights, it is essential to recognize that personal finance can be highly complex and unique to each individual. A financial advisor provides professional expertise and personalized guidance to help you make well-informed decisions tailored to your specific circumstances and goals.

Beyond offering knowledge, a financial advisor serves as a trusted partner to help you stay disciplined, avoid common pitfalls, and remain focused on your long-term objectives. Their perspective and experience can complement your own efforts, enhancing your financial well-being and ensuring a more confident approach to managing your finances.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Readers are encouraged to consult a licensed financial advisor to obtain guidance specific to their financial situation.